PP: A Simple Overview of The Energy Industry

PP: A Simple Overview of The Energy Industry

Welcome to the 82nd Pari Passu Newsletter.

Today, we are learning more about one of the most underrated industries of current times: energy. From its impact on everyday life to its relation to international conflicts, energy is one of the most influential and important industries of the broader economy. Interestingly enough, energy makes up no more than 7% of the US GDP and it is often overlooked by young professionals (myself included) who would rather spend their time on other verticals.

In today’s newsletter, we will be taking a closer look into the energy industry: its major players, historical market performance, future outlook, and much more.

But First a Message from Today’s Sponsor:

Bankruptcy Data for Financial Advisors

News. Alerts on newly distressed corporates based on ratings agency downgrades, going concern warnings, distress bond trading and more.

Courts. Follow reporting on on-going bankruptcy cases, dockets and new filing alerts.

Data. Research restructuring plan mechanics and class recovery consideration and rates, terms of DIP and exit financings, and asset sale bids.

Documents. Search across all bankruptcy court dockets for key words or document types, and set up alerts to track future matches to your search.

Business Development. Research and activate email updates on involvements of any advisor or party of interest appearing across the distress universe.

Track. Follow any company, creditor, advisor, document type or search term to receive real-time alerts to your areas of interest.

Part 1: Industry Overview

The energy industry is a global industry responsible for discovering, extracting, and providing energy resources. These resources consist of non-renewable fossil fuels (oil, petroleum, gasoline, natural gas, etc.), nuclear energy, and renewable energy (hydropower, solar power, wind power, etc.).

In 2022, approximately 79% of the US’s energy came from fossil fuels, 8% from nuclear, and 13% from renewables. More specifically, oil (petroleum) and natural gas made up 36% and 33% of U.S. energy consumption respectively. Within renewable energy consumption, the source with the highest percent consumption was biomass energy, at 37% [4].

The energy industry can be broadly divided into three main sectors: fossil fuels, renewable energy, and nuclear energy. Although companies in these three sectors are all considered energy companies, they differ in numerous ways given their specialization in different energy resources.

Fossil Fuels

Fossil fuels have long dominated the energy industry. With fossil fuels contributing nearly 80% of the U.S.’s energy supply and 77% of the world’s supply in 2022, human dependence on fossil fuels is undeniable. Within the fossil fuel industry, there are three primary classifications: oil, natural gas, and coal. Due to the high demand for oil and gas, fossil fuel companies have grown very large in recent decades. Top companies in the field by market cap include Exxon Mobil at $500bn, Chevron at $300bn, and ConocoPhillips at $130bn [7] [8].

However, no entity has more influence in the fossil fuel industry than the Organization of the Petroleum Exporting Countries (OPEC). OPEC is an international organization founded in 1960 by the key petroleum exporters meant to regulate the supply and price of oil. OPEC is effectively a cartel that controls the world’s oil supply, with virtually unchallenged control over the price of oil [9].

Fossil fuel’s dominance in the industry can be attributed to two reasons: accessibility and efficiency. Fossil fuels are, by far, the most easily accessible and abundant energy resource. For decades, humans have exploited the Earth’s huge fossil fuel reserves. Furthermore, fossil fuels are also energy-dense, meaning they are efficient for producing large amounts of energy. The oil and gas sector alone generated an astronomical $4.3tr in revenue in 2023 [10].

Renewable Energy

While renewable energy represents a significantly smaller portion of the energy industry, it is the fastest-growing sector. From an accessibility and efficiency standpoint, renewables are largely unable to compete with fossil fuels. Renewable infrastructure still needs years of development and current renewable technologies are not advanced enough to drive down the price of renewable energy. However, fossil fuels have two key flaws: 1) fossil fuel reserves are finite and will eventually run out, and 2) fossil fuels contribute massive amounts of carbon emissions into the atmosphere, which is unsustainable from an environmental perspective.

Since the COVID-19 pandemic, global renewable energy investment has seen a huge improvement. Global energy investment in clean energy has grown by a compounded annual growth rate of nearly 10% from $1.2tr in 2019 to $1.7tr in 2023. This growth is unique to the sector – fossil fuel investment saw a slight 1.5% decrease during the same period. Furthermore, since 2015, investment in renewables has grown by a CAGR of ~6% while investment in fossil fuels has fallen by a CAGR of ~3%. These trends in data indicate that major changes within the energy industry are imminent over the next few decades [11].

Within the renewable energy sector, the key classifications are the traditional three renewable energies – solar, wind, hydroelectric, and biomass energy. In 2022, 29% of renewable energy came from wind power, 18% from hydroelectric, 14% from solar, and 37% from biomass. The most promising sectors are solar and wind energy, given the sheer abundance of its resources. In fact, the Earth’s atmosphere receives enough solar energy in an hour to meet the annual electricity demand of every human being. The challenge, however, is harnessing that energy [12] [14].

Nuclear Energy

Nuclear energy is another type of “alternative” energy source that has the potential to help replace fossil fuels. Currently, there are 439 nuclear reactors in thirty-one countries in service, meeting approximately 10% of the world’s energy demands. Nuclear energy is generally classified as a clean energy source since it produces energy through a zero-carbon emissions process. However, nuclear waste is a byproduct of the process, which is often pointed out as a critique of the resource [15].

Nuclear energy is by far the most energy-efficient resource. In fact, nuclear fission, the process by which nuclear energy is harnessed, is nearly 8,000 times more efficient at electricity generation than traditional fossil fuels are. Unfortunately, nuclear energy is plagued by high fixed costs and poor public opinion, and therefor3 energy companies have been largely reluctant to venture into the space [13].

Part 2: Financial Performance

Energy Landscape

At the apex of the energy landscape are the top fossil fuel companies. These include companies such as Exxon Mobil, Chevron, and ConocoPhillips, all of which are major players in the oil and gas industries. Globally, the largest oil and gas company by market cap is Saudi Aramco, with a market cap of $1.94tr. Compared to its U.S. “rivals”, Saudi Aramco dominates the industry, generating significantly higher earnings and operating margins. For example, in 2023, Saudi Aramco generated $240bn in earnings before taxes and an impressive operating margin of 50%. Its closest American competitor generated $53bn in earnings and a lackluster margin of 20% [16].

Renewable energy companies are much smaller in size compared to their fossil fuel counterparts. Key players in the field include First Solar at $27bn and Enphase Energy at $15bn. Interestingly, many companies in the renewable energy space are considered technology companies, as their core focus is the development of technologies that help harness renewable energy [7].

At the bottom of the energy pyramid in terms of market cap are nuclear energy companies. The largest pure-play company in the space is Uranium Energy at $2.5bn. However, this is because energy companies solely focused on nuclear energy are rare. As such, the top companies listed in this space are primarily uranium mining and processing companies. Nuclear energy production companies are usually larger energy companies that have a specialized nuclear energy arm. For instance, the largest nuclear plant operator by electricity capacity in the U.S. is Constellation Energy Corporation, a $60bn market cap company that focuses generally on natural gas and carbon-free energy [7].

Performance by Sector

Energy stocks have displayed positive but slow growth in 2024, rebounding from a poor year in 2023. In the last six months, the Thomson Reuters U.S. Energy ETF and iShares U.S. Energy ETF each grew by 6%, whereas the S&P 500 saw a 15% return over the same period [7].

Fossil fuels have displayed varied performance in 2024. The Thomson Reuters U.S. Fossil Fuels Index is down 12% since January. However, the Brent Crude index and API2 Rotterdam Coal Futures are up 10% and 7% respectively during the same period. Henry Hub Natural Gas Futures are up 5% [7].

Renewable stocks, on the other hand, have been suffering. Since January, the Thomson Reuters U.S. Renewable Energy Index is down 20%. This underperformance is likely the result of a weaker global economy and sustained higher rates, which makes borrowing money less attractive for capital-intensive renewable energy projects [7].

Energy Select Sector SPDR Fund ETF

The Energy Select Sector SPDR Fund ETF (XLE) is an energy ETF that aims to correspond to the price and yield performance of the Energy Select Sector Index. This index is meant to provide a representation of the energy industry of the S&P 500, and includes oil, gas, and affiliated companies. The performance of the XLE ETF is often a reflection of the performance of the overall fossil fuel market [20].

As of June 24th, the ETF sits at a price of $91. XLE’s top holdings include Exxon Mobil at 27%, Chevron at 17%, and ConocoPhillips at 8%. This closely mirrors the holdings and weights of the index. The fund industry allocation is 91% oil, gas and consumable fuels and 9% energy equipment and services, meaning it focuses solely on the fossil fuel industry [7] [20].

It is quite apparent that XLE is not a diversified fund, with the top two integrated major oil and gas companies representing over 40% of the fund’s holdings, and the other twenty-one holdings representing the remaining 60% of the fund. Additionally, the large majority of the fund is invested in the same sector. Despite this lack of diversification, the fund has done quite well betting on the fossil fuel industry. In terms of performance, the ETF has provided a ~8% return after taxes since its inception in December 1998. Its ten-year return is ~4%, five-year return is ~15%, and one year return is ~26% [20] [21].

Valuation Methodology

Oil, gas, and natural resource companies often require valuation methodologies that differ from traditional methods. This is because these companies are dependent on commodity prices, namely the price of their respective resource. However, not all oil and gas companies are valued the same. Here is a list of the general classifications for oil and gas companies [17]:

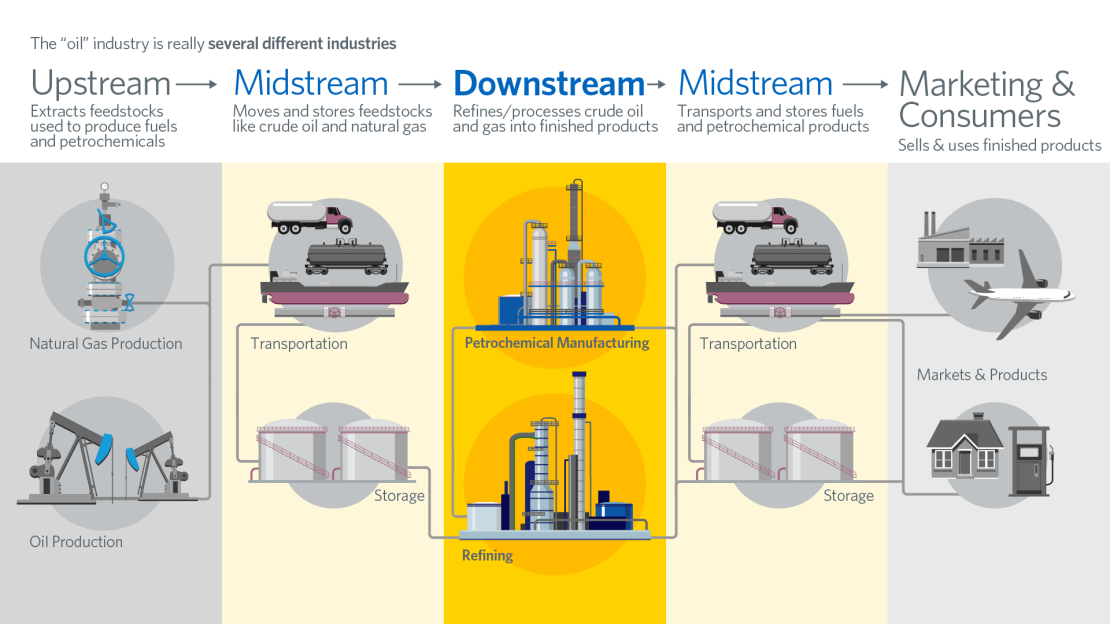

Upstream companies: Also known as exploration & production (E&P) companies, these firms focus on locating and extracting resources from the ground.

Downstream companies: These firms focus on refining extracted resources and transforming them into marketable products, such as jet fuel or automobile gasoline.

Midstream companies: These firms act as intermediaries between upstream and downstream companies, focusing on the transport of extracted resources.

Oil field service companies: These are companies that provide third-party services, such as oil field maintenance and repairs.

Integrated majors: These are large-cap oil and gas companies that have vertically integrated the entire process into their business model (ex. Exxon Mobil).

E&P companies are often the most tricky to value. Here are the key reasons why this type of oil and gas companies warrant different valuation methodologies [17]:

Absence of price control: Oil and gas companies cannot control prices / revenue. Since global oil and gas prices are determined primarily by the laws of supply and demand, which is heavily influenced by OPEC, individual firms have no control over the pricing of their products.

Balance sheet-centric: The balance sheet is the most important financial statement, due to the dependence oil and gas companies have on their assets. This is because fossil fuel reserves are considered assets, so the amount of such reserves largely determines the company’s future performance.

Depleting assets: Assets typically increase as a company grows. However, as an oil and gas company increases its revenue, this means its assets likely decline because the company is using up its revenue-generating fossil fuel reserves.

As such, the value of an E&P company is largely determined by the value of its reserves, its primary asset. Reserves are classified into two primary categories: proved and unproved reserves. According to global advisory firm Stout, “proved reserves are quantities (volumes) of oil or natural gas that are recoverable in future years from known reservoirs under existing economic and operating conditions”. Unproven reserves are either probable reserves, which are equally likely to contain quantities of oil/gas higher or lower than estimated, and possible reserves, which have a 10% probability of containing quantities higher than estimated. By accurately assessing the value of an E&P company’s reserves, a discounted cash flow model can be applied to the reserves to create a reserve report [18].

E&P companies may also be valuated through comparable transactions or comparable companies analysis (comps). As we all know, this type of valuation is not unique to E&P companies and is often used to value privately held companies. However, a major difference in E&P comps is the use of EBITDAX rather than EBITDA for most other businesses. EBITDAX is a company’s EBITDA before the exploration costs necessary for successful efforts. This is because exploration costs are often baked into depreciation costs, so EBITDAX equalizes the accounting [18].

In order for comps to be effective, the selection of appropriately comparable companies is very important. Important screening criteria include company size (market cap or reserve volumes), percent oil/gas, reserve life (proved reserves divided by the previous year’s production), ratio of proved undeveloped reserves (PUDs) to total provided reserves, and geographical area of operation. After comparable companies are screened, important metrics that are evaluated include enterprise value (EV), EV/ daily production, and EV/EBITDAX (as opposed to EV/EBITDA). Additionally, other common multiples used to value E&P companies include EV / proven and probable reserves and price/cash flow per share [18] [19].

Conventional valuation methodologies, such as DCF and comps analysis can usually be used for midstream, downstream, and oil field service companies. These companies, as opposed to E&P companies, function with less dependency on assets such as reserves, and thus can usually be accurately valued with conventional methods [18].

Part 3: Energy M&A

M&A activity in the energy industry has been particularly high in recent years. In 2022 alone, there were 1,241 M&A transactions, the highest annual total ever. Additionally, in 2023, a number of blockbuster acquisitions took place:

ExxonMobil acquires Pioneer Natural Resources for $60bn, October 2023

Chevron acquires Hess for $53bn, October 2023

Occidental Petroleum acquires CrownRock for $12bn, December 2023

Specifically, many of these acquiring companies are looking to lay a stake on land in the Permian Basin, a large sedimentary basin located in western Texas. The Permian is the largest petroleum-producing basin in the United States and has produced a cumulative 29bn barrels of oil and 75tr cubic feet of gasoline. In the basin’s Wolfcamp and Bone Spring Play formations alone, there sits an estimated 50bn barrels of crude and nearly 300tr cubic feet of natural gas. Furthermore, if the prices of oil and gasoline do increase, companies may be more willing to extract previously economically unattractive resources [2].

Each of these deals reflects the growing trend of larger companies aiming to acquire more land to extract fossil fuel resources from. As the world’s fossil fuel reserves continue to wane, fossil fuel energy companies are rushing to grab up as much energy-rich land as possible.

The consolidation is also concerning. According to a PwC 27th Annual Global Survey, about 24% of global energy CEOs were concerned about their company’s exposure to climate change. The proportion of concerned energy CEOs was higher than any other sector. Not only is the possibility of running out of fossil fuels an issue, but climate change is another dilemma that the energy industry faces in the coming years.

However, acquisitions are not the only trend in energy M&A. For many companies unable to partake in multibillion-dollar acquisitions, divestitures have been the strategy. A survey of M&A practitioners found that nearly “80% of energy industry respondents have proactively evaluated separating or spinning off parts of the business”. Within the first nine months of 2022, energy divestitures totaled $250bn, more than any other industry.

Companies unable to consolidate and remain competitive have been racing to get rid of their carbon-heavy assets in preparation for the transition to renewable energy. Enel, an Italy-based global energy company, sold assets valued at $21.5bn to streamline its business and focus on electrification. TotalEnergies, an oil and gas company, spun off its Canadian operations in order to align with its new low-emissions strategy [3].

Here, we can see a divide in global energy M&A strategy. On one side are energy giants, focusing on scale M&A by acquiring similar companies in order to access their land resources. On the other side are smaller energy companies, focusing on more scope-based M&A in order to expand their portfolio and remain competitive during the energy transition. Each strategy has its own pros and cons:

Scale M&A: This strategy enables companies to increase their competitive advantage in the consolidating fossil fuel landscape. It allows companies to acquire more resources for profit while simultaneously removing competition from the field. However, scale-based acquisitions are more short-term focused and do not necessarily benefit the company in the long-run [1].

Scope M&A: This strategy allows companies to increase the scope of their operations, essentially widening their functionality in the market. Scope M&A focuses on generating revenue synergies with deals that occur outside the acquirer’s core business, making this type of M&A much riskier. There is no guarantee that expected synergies will turn out to actually occur. In fact, the most common reason that M&A deals fail is due to over-estimated revenue synergies. However, scope-based acquisitions are more long-term focused, enabling companies to ease into the global energy transition [1].

Interestingly, some companies are partaking in both scale and scope M&A. Take ExxonMobil for example. After its blockbuster deal to acquire Pioneer in October 2023, the company announced plans to become the leading producer of drilled lithium in Arkansas a month later. While the Pioneer deal was primarily a scale-based deal, the lithium plans are scope-based, enabling Exxon to reposition for the future. Other companies are doing the same: General Motors announced a $650mn investment in Lithium Americans to develop a Nevada lithium mine; Ford Motor Company signed new lithium offtake agreements; Tesla signed an agreement with Magnis Energy to supply anode materials for batteries [1].

Part 4: Future Outlook

Opportunities

The future of the energy sector is both exciting and unpredictable. With fossil fuel reserves running out, the need for renewable energy has never been greater. However, with this transition comes the opportunity for new innovation and technologies to blossom.

While most people are aware of the current renewable energy options, such as hydropower, solar power, and wind power. A lesser-known renewable option with immense potential is hydrogen energy. Hydrogen energy is classified based on how the hydrogen is sourced. The preferred form of hydrogen energy is green hydrogen, which is produced through the process of electrolysis, the process of separating the hydrogen and oxygen atoms in water. It is highly attractive given that it can be infinitely sourced, has zero carbon emissions, and is an efficient and highly energy-dense source [4].

Lithium batteries are also an important future market for energy companies. With their growing applications in products such as electric vehicles (EVs), many energy companies have already begun investing in the lithium production process. Laying a stake early on will enable these companies to profit later on [1].

A wild card in the future of energy is nuclear fusion. While the proliferation of nuclear fusion technology is still years away, fusion represents a golden solution for the industry. Fusion has the potential to produce immense amounts of energy with essential zero carbon emissions, more efficiently than fission currently can. Additionally, compared to nuclear fission, fusion does not create radioactive waste as byproducts [1].

Challenges

The energy industry has a puzzling dilemma to solve: support the immense energy needs of the world with a sustainable source. Unfortunately, fossil fuels are no longer the solution to that dilemma. Not only are fossil fuels unsustainable, they are simply running out. And, given our current abilities to produce renewable energy, there exists no solution to the energy dilemma.

The effects of fossil fuel consumption should not be overlooked. In 2018, nearly 90% of global carbon emissions came from fossil fuel consumption. Many of the consequences of global warming, from increased global temperature, increased occurrence of natural disasters, melting ice caps, and rising sea levels, are being perpetuated by the fossil fuel industry. If these resources continue to be exploited, the damage may become irreversible [6].

Addressing these concerns will be a great challenge for the energy industry. As grim as it sounds, if the energy industry fails to do so, the future of the human race might be in jeopardy.

Sources: [1], [2], [3], [4], [5], [6], [7], [8], [9], [10], [11], [12], [13], [14], [15], [16], [17], [18], [19], [20], [21]

Interested in our updated reading list? Check it out here.

Got Feedback? Just hit Reply. Seriously, I would love to get your thoughts.

Interested in our IB / PE / Finance course recommendation? Check it out here.

Looking for more Pari Passu Content? Check out Instagram | Twitter | Linkedln