The Holy Grail - Permanent Capital Vehicles

The Holy Grail - Permanent Capital Vehicles

Welcome to the 79th Pari Passu Newsletter,

After a restructuring write-up last week, we are back with a generalist investing lesson today: the rise of permanent capital vehicles.

At a high level, investing roles entail deploying the limited partners’ capital into the opportunity that offers the highest risk-adjusted return. Behind this apparently simple description, there are a myriad of technicalities that enable a check to be wired in exchange for an ownership stake (both in the public and private markets).

Today, we are diving into the evolving relationship between the limited and general partners and the shift toward permanent capital vehicles.

But first, a message from Piece of Cake Moving & Storage

Make your next moving day a Piece of Cake, with America's most loved mover Piece of Cake Moving & Storage. Use the promo code IGFAMILY for a 10% discount off your next local move, or a 5% discount off your next out-of-state long distance move.

This moving promo code never expires and can be used for all your upcoming moving days! Whether you're moving locally or out of State, Piece of Cake Moving offers extensive moving day services including; White Glove Packing & Unpacking, Short and Long Terms Storage, as well as Moving Box Bundles, and a convenient Plastic Bin Rental Service.

Get a Free Flat Fee Moving Quote and use the code IGFAMILY.

Introduction

When one of the most successful financial products ever, the leveraged buyout (LBO), was initially pioneered by Henry Kravis and Teddy Forstmann in the 1970s, it was initially a burdensome process. Raising money from investors to finance the equity portion of an LBO was conducted on a deal-by-deal process, requiring additional time and energy for each deal. As LBO specialists grew and evolved into powerful firms such as KKR and Forstmann Little & Company, they established longer-term investment structures to secure capital commitments from Limited Partners (LPs), such as endowments, pension funds, and sovereign wealth funds, to finance the equity portions of LBOs. These structures, which are technically known as blind pools, allow a limited partnership to raise funds without telling investors where the money will be specifically allocated. Blind pools, referred to publicly by their individual vintage fund name (e.g., KKR Flagship Fund XIII), typically retain secured capital commitments for ten years. This additional firepower gave these firms a competitive advantage, allowing them to react rapidly to business developments without needing to go out and raise new capital. For example, it allowed Kravis and Forstmann to continue raising the price offered to management during the famous 1988 bidding process for RJR Nabisco. In addition to speed, this ten-year structure also theoretically gives the private equity firm, or General Partner (GP), the time to comfortably source, study, and invest in companies it decides are good investments at the time it deems ideal for maximizing returns, with the confidence that capital is lined up [2].

While vintage funds have been wildly successful and remain the standard fund structure, there have been several developments that have led private equity firms to look elsewhere. The first of these was the Great Financial Crisis (GFC), which led to the extinction of a quarter of buyout firms post-2008. Massive investments made pre-2008 at expensive multiples significantly underperformed, a major blow to an industry that had been given an increasingly large share of global capital without question. This made it much more difficult for firms to raise subsequent funds post-2008. Even leading megafunds such as TPG Capital had a difficult time fundraising. It took TPG eight years to close a new flagship fund, on the back of underperforming transactions such as the buyouts of Harrah’s Entertainment (alongside Apollo), TXU, and Washington Mutual. A trend echoed across the industry: when TPG finally raised its $10.5bn 2016 vintage, it was about half the size of its 2008 vintage, TPG VI [2].

Another major development was the commoditization and saturation of the industry over the past decade in a low-interest environment. With private equity firms raising increasingly larger funds with less time between raises, competition for LP dollars became even more intense, with more time and resources allocated to fundraising. With the further standardization of investment techniques, from covenant-light financing to vendor due diligence, equity returns have constrained and LBOs have become more accessible to generalists. Many LPs have themselves elected to make direct investments rather than relying upon the private equity firms (the general partners, or GPs). Part of the reason for the power shift from GPs to LPs has also been that the majority of GPs do not return LP commitments within the contractual ten years. Additionally, as time has passed, firms that have had a long history of top quartile funds have eventually had misses, leading to decreased LP interest. While a handful of firms with immaculate track records or unique investment edges still have the ability to dictate terms with LPs and charge fees above-standard fees, the majority have experienced more difficulty in differentiating themselves to LPs [2].

The final critical development encouraging private equity firms to look beyond the vintage fund structure has been the IPOs of many leading firms. Following Blackstone’s IPO in 2007, a number of firms have followed, most notably Apollo, Ares, Carlyle, KKR, and TPG. While private equity firms were previously incentivized to raise larger and larger funds that achieved high rates of returns in order to be compensated through their share of the growing returns, known as carried interest, or “carry,” the IPOs changed this. Instead, management of the private equity firms could be compensated through stock in the publicly listed firm. Additionally, beyond the interests of LPs, firms now had to consider the interests of the public shareholders. Due to the variability of fundraising and investment performance through the vintage model, public shareholders have awarded higher multiples to PE firms not based on the carry generated by investments, but instead on management fees charged to LPs for the assets managed on their behalf. As a result, the management of publicly traded PE firms are incentivized to increase the scope and duration of the assets they manage in order to charge these consistent, growing management fees, de-emphasizing the former importance of the traditional vintage fund model [2, 6, 8].

Growth in PCVs

Given these three developments, private equity firms became massive asset managers and began to ask a new question. Could they develop a new fund structure that would allow for consistent fee generation over a much longer time horizon? This would help minimize pressure around investment timing, reduce or eliminate the need to continuously raise fresh capital from LPs, and boost valuation multiples for their firms. In theory, perpetual capital, or investment funds with an indefinite life and flexible exit timelines, could be this silver bullet. Once the money has been raised, the investment manager could have the right to charge annual fees and continue to invest the capital forever [1, 6, 8].

The first major push into permanent capital by the asset managers has been through various permanent capital vehicles, or PCVs, which typically target internal rates of return of 10-14% annually (versus 20%+ for traditional private equity). While limited-life private investment funds have a ten-year term before liquidation, PCVs can go past 15 years with some periodic extensions, typically providing several arrangements to make liquidity available for investors. While PCVs are thought of as a newer invention, they have existed for a long time in various forms. For example, real estate investment trusts (REITs), Master limited partnerships (MLPs), publicly traded limited partnerships, variable funds (e.g., life insurance and annuities), and closed-end funds (a type of mutual fund) are all types of permanent capital vehicles [1, 4].

The asset managers have taken different approaches to PCVs in their quest to circumvent LPs and traditional limited-life private investment funds. One approach, which Blackstone has embraced, is to appeal to the huge number of qualified purchasers, or retail investors with at least $5mm in investments that have historically not had access to PE and Credit as an asset class but are comfortable investing in a longer-dated offering. Blackstone now provides these individuals with three offerings consisting of BREIT, which invests in real estate, BCRED, which invests in credit, and Blackstone Private equity strategies, which co-invests alongside all of Blackstone’s private equity strategies (buyout, growth, infrastructure, life sciences, and preferred equity). Unlike previous Blackstone limited-life private investment funds, these funds are structured as a non-traded REIT, non-traded business development company (BDC), and an evergreen fund, respectively, giving them the ability to continuously take in and distribute money [8, 9, 10, 11].

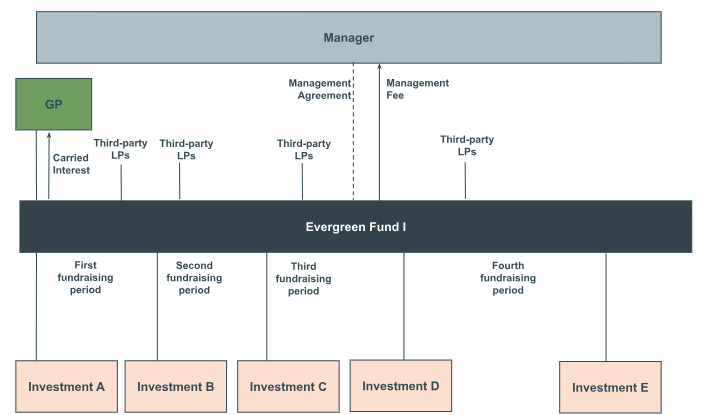

For the evergreen fund, the recently launched Blackstone Private Equity strategies, investors will largely be at the mercy of the GP, Blackstone. For reference, the traditional structure of an evergreen fund is depicted below. Over time, existing or new LPs provide additional capital to the fund, and will also redeem capital. However, the fund will never fully redeem investors at once, unless the fund is required to do so after a very long time. There are two possible variations related to the investments themselves. In the first, existing investors are diluted so that all investors participate in all investments (with consideration given to appropriate pricing). In the second, existing investors are not diluted, as new investors only participate in forward investments. Likewise, capital calls typically are the same as traditional vintage funds, functioning on an as-needed basis. However, this is different for Blackstone’s fund, which called the capital up front. While the remaining terms of Blackstone’s fund are not entirely public, investors will be allowed to request the value of their investment back at any point. However, total fund redemption is limited to 3% of assets per quarter. The only possible exit is through a sale back to Blackstone, as no secondary market is ever expected to exist for this fund. Effectively, the fund is still an experiment to determine if both the evergreen structure and retail client base can function effectively and scale [9, 10, 11, 12].

Source: White & Case

An alternative approach, first inspired by Buffett's Berkshire Hathaway’s use of auto insurer GEICO to provide a dependable source of funds, has been Apollo’s development of an insurance solutions business, which invests capital for insurance companies on their behalf. Apollo feeds this business line capital from Athene, a life insurance provider it fully purchased in 2022. Given that insurance companies take in money from their stable client base continuously, invest it, and return certain amounts later, the insurance model has proven to be an excellent source of permanent capital. KKR has also pursued this path, recently acquiring insurer Global Atlantic in 2023, and Blackstone currently maintains a partnership with Resolution Life [4, 5, 6, 7, 8, 10].

State of PCVs Today and Future Outlook

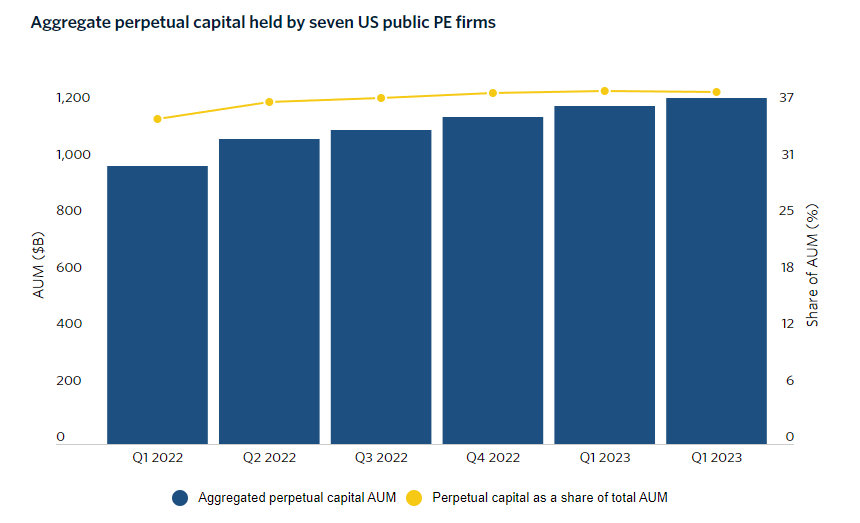

In 2023, there was an industry-wide slowdown in private equity fundraising. However, Blackstone, Apollo, and KKR all saw their assets under management, or AUM rise, thanks to perpetual capital. At the end of 1H 2023, perpetual capital in the hands of the seven publicly traded private equity giants surged by 13.2% YoY, totaling ~$1.2T. This exceeded the growth rate of these firms’ total AUM, which grew ~10% over the same period [6].

Source: Pitchbook

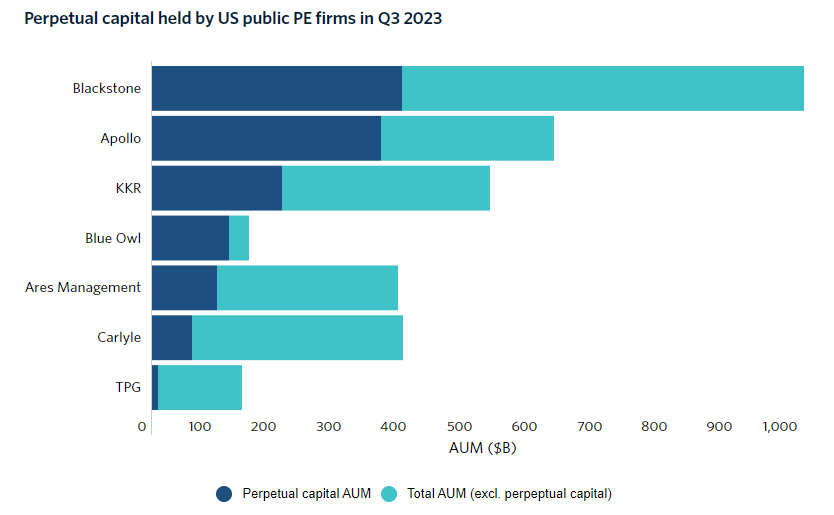

Source: Pitchbook

As the second graph demonstrates, different asset managers have embraced perpetual capital to varying extents. While Blackstone, Apollo, and KKR have made it a central part of their growth strategies, Carlyle and TPG have not. Permanent capital strategies are still a work in progress. This was clearly demonstrated when BREIT, Blackstone’s retail real estate fund, faced mass investor redemption requests to remove their money simultaneously as interest rates rose in 2022, forcing Blackstone to limit redemptions. However, despite hiccups, it is ultimately probable that perpetual capital will continue to grow in importance. Both retail offerings and insurance solutions will play a critical role as asset managers seek to source consistent capital in order to prioritize stable fee generation. While it is difficult to predict the future pace of growth for perpetual capital’s capture of AUM shares, the historical vintage fund model could someday be a thing of the past for the next generation of private equity investors [5, 6].

Sources: [1], [2], [3], [4], [5], [6], [7], [8], [9], [10], [11], [12]

How did you like this week’s Pari Passu? Loved | Great | Good | Meh | Bad

In case you missed the latest Pari Passu Newsletters:

Interested in our updated reading / wellness list? Check it out here.

Got Feedback? Just hit Reply. Seriously, I would love to get your thoughts.

Interested in our IB / PE / Finance course recommendation? Check it out here.

Looking to reach 8,500+ investors, bankers, lawyers?

Looking for more Pari Passu Content? Check out Instagram | Twitter | Linkedln