Two Examples of Interview Restructuring Cases

Two Examples of Interview Restructuring Cases

Investing, Banking, Restructuring, Podcast Summaries, and Niche Finance Topics

Welcome to the third Restructuring newsletter,

Today, we will have a bit of a different post in which we will go through two cases that can be really helpful to prepare for any level of restructuring interview.

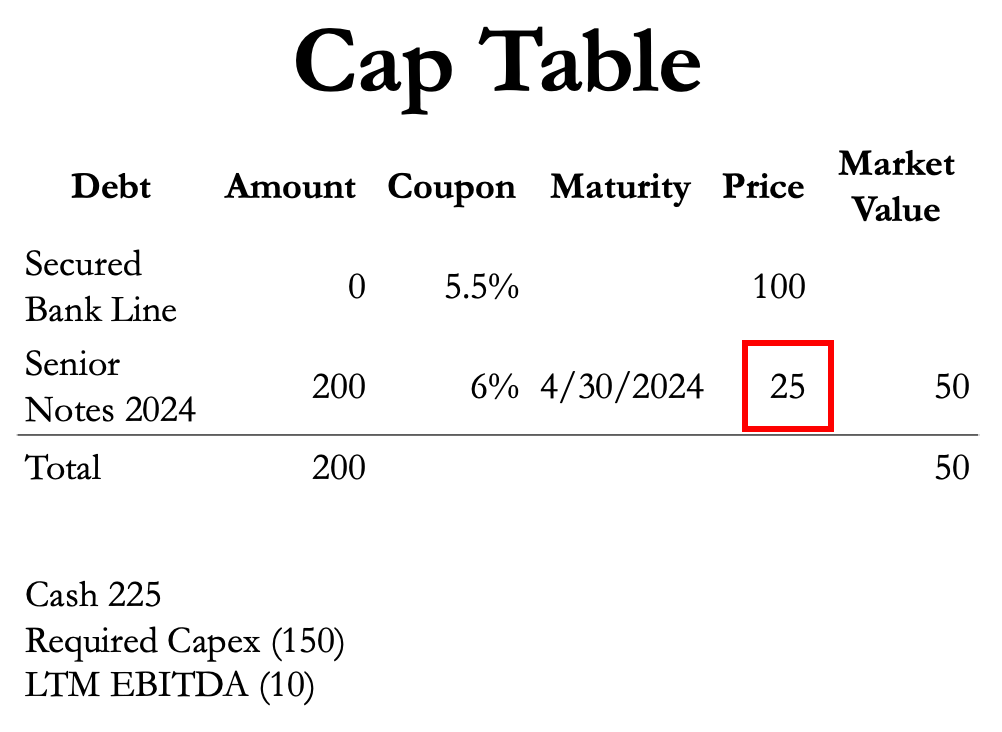

Basic Restructuring Case

ABC is an Internet company with $225 in cash and $1000 in historical investment in various Internet ventures that have modest negative operating cash flow. To mature these businesses to the point that they have value potential will require further investment of at least an additional $150 in total.

ABC’s only credit liability is $200 in 5% subordinated convertible notes maturing in two years. Its formerly high-priced stock (peak value $200 per share) trades at under $1 a share and the notes are trading at 25 because the market is skeptical whether or not the firm’s various negative cash flow businesses have value.

For simplicity, assume notes have no covenants, and ABC’s cash position essentially ensures there will be no payment default until maturity.

What would you advise the company to do?

Answer:

Perfect-world scenario for Note Holders

The note holders would likely prefer that ABC file an immediate chapter 7 liquidation and, depending on the drag of administrative expenses and trade claims versus the liquidation value of the operating investments, take the $225 in cash for a par recovery. Given the market price of 25, this would be great! But, unfortunately, the note holders, absent a default, have no power to force a bankruptcy, and such a scenario does nothing for management and the existing equity.

Perfect-world scenario for Management

Management’s perfect-world scenario is to continue with the business plan because, given its genius (a.k.a. ego) and the turn in the marketplace that, in management’s view, is just around the corner, the market is likely once again to recognize ABC’s true potential. When that occurs, the stock will go up, members of management will get rich from the new $1 options they have awarded themselves, and a refinancing or asset sale will be used to repay the maturing debt.

The collapse of the stock price may prompt management to consider share repurchases, which would result in an erosion of the notes’ asset support, that the note holders will be powerless to prevent because there is no restricted payment covenant in the notes’ weak indenture. If management is wrong, ABC will squander its cash and likely will have to file for bankruptcy when the notes mature in two years.

Realistic Alternatives

These are two possible scenarios, but assuming management is acting at least semi-rationally in its, and hopefully the shareholders’, interests, there are other more probable and mutually beneficial scenarios. Management should realize that in a bankruptcy, the equity is likely to be wiped out and they will be out of jobs and humiliated. Therefore they will want to avoid or at least minimize the worst-case consequences of that scenario. Some possibilities to explore include:

1. Buy back notes at a discount

A fairly obvious strategy is to buy back the notes at a discount. Since the market value of the notes is only $50, there is a strong argument to use some of the $225 in cash to purchase them at the discount and use the remaining funds for the business plan. It is important to remember that, when the market realizes the that firm is engaging in repurchases, the notes’ price will rise.

Nonetheless, at a 25 price level, a note buyback is compelling. The aggregate amount to spend, the price to pay, and the trade-off versus further investments in the business will be variables in a difficult calculus, but repurchase of notes is a clear first step.

2. Asset sale

Alternatively, selling assets could provide additional liquidity. Monetizing assets, assuming “fair prices” can be realized, would be a desirable course for the notes.

3. Additional financing

Otherwise, management may also consider trying to obtain additional financing. The loan would have to be done on a secured basis because, practically speaking, no lender would make an unsecured loan to a firm where the existing market perception of the borrower’s risk is such that its debt trades at 25. Even on a secured basis, it is unclear whether any lender would be interested in such a financing unless the primary collateral is the cash. In that case, management would not have derived much benefit, spent money and time in arranging the financing, and, given the covenants demanded by secured lenders, limited its operating flexibility. From a note’s perspective, if a secured lender had a pledge of all the assets including the cash, the notes would clearly be worse off. Since it is not obvious why the company would benefit from such a borrowing, this alternative is not likely to be pursued.

4. In-court process

As management looks out to the maturity of the bonds, it should be planning for the probability, or at least the possibility, that unless the market really does rebound, ABC will not have the resources for repayment. In that case, on the basis of the limited facts given, it does not appear that a bankruptcy would add value (through lease rejection, few on- and off-balance-sheet liabilities etc.) to the enterprise, and thus its inherent costs would only burden the potential recovery, tenuous as it may be, of the equity.

Summary

Therefore, in the “no market recovery” scenario, the endgame should be some type of out-of-court exchange proposal in which the notes are given the vast majority of the equity, but the existing shareholders retain a sliver. A well-conceived and well-executed exchange would also give management executives a de facto opportunity to make amends with the bondholders in an effort to preserve their jobs. There could, of course, be many other scenarios, but these, are the most probable.

When asked these ”cases” questions in interviews, it is important to show you are able to consider the different alternatives a company can explore and the potential advantages and disadvantages of each path. This example was very simple and provided a quite straightforward solution, but in practice, things get complicated very quickly. Reading about current cases is the best way to try to understand the different options companies consider.

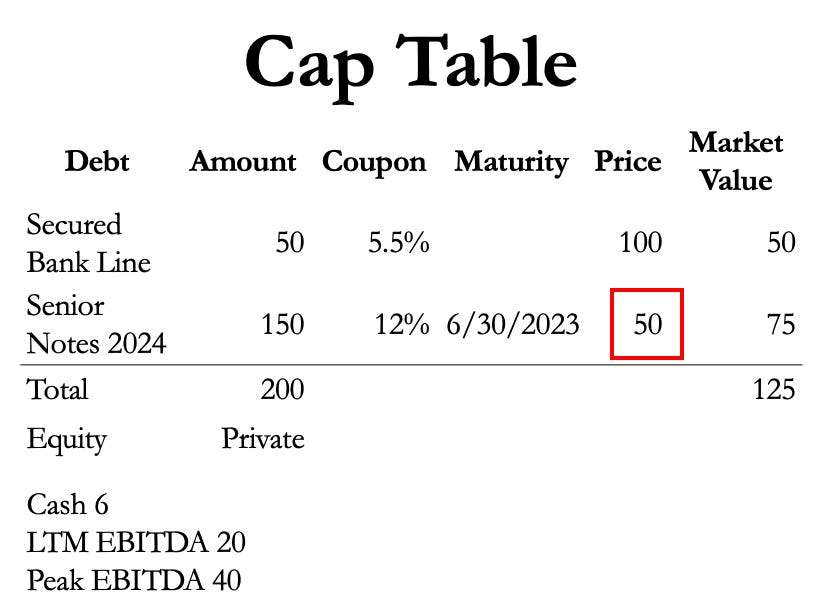

Intermediate Restructuring Case

XYZ, which is owned by a well-regarded PE fund, is involved in several segments of the specialty steel business. The economy is weak and revenues are down. Because of the relatively high fixed-cost nature of the business, earnings before interest, taxes, depreciation, and amortization (EBITDA) is down even more severely. In fact, LTM EBITDA, $20, is a six-year low (peak EBITDA was $40). The capital structure is fairly simple: $50 drawn on a secured bank revolver and $150 in 12% unsecured senior notes that mature in one year. These notes trade at 50. Liquidity is limited: cash is down to $6 and there is a technical default on the bank line. A $9 bond coupon payment is due in two weeks. XYZ’s 3 industry peers are also exhibiting weak performance. One has filed for bankruptcy protection. The other two are likely to survive and are trading at enterprise value/EBITDA multiples of 6x and 7x, respectively.

What would you advise the company to do?