An Overview of the Pharma Sector

An Overview of the Pharma Sector

Welcome to the 93rd Pari Passu Newsletter,

After the amazing success of last week’s edition about Triple Dip, this week we are learning more about an industry: pharma. With the global pharmaceutical market projected to reach $2.36tn by 2030, pharma is one of the most important and influential markets in the economy. At the same time, Pharma is also one of the most controversial, with top firms facing constant criticism for their immoral pricing strategies and lack of transparency.

In the article below, we will cover this industry: its origins, major players, market performance, key criticisms, and much more. This is a fascinating sector that most of us rarely interact with, so I hope this write-up will have many lessons.

Curious how the world’s best investors are using AI

Hebbia works with lean leading credit and restructuring shops.

Hebbia can summarize a credit agreement, draft one-pagers based on your team’s investment philosophy and so much more.

Book a 20 minute demo to see why they work with 1/3 of the 25 largest alternative asset managers.

Origins and History

The origins of the pharmaceutical industry date back to the Middle Ages, when medieval apothecaries and pharmacies offered traditional remedies based on folk knowledge rather than science.

It would not be until the Industrial Revolution that major advances in the field would be made. German company Merck, founded in 1668, would be one of the first companies to move towards a scientific approach to pharmacy. This occurred in 1827 when Heinrich Emanuel Merck began a transition towards scientific concern by manufacturing and selling alkaloids [9].

In America, the pharma revolution also occurred during the early to mid-19th century. Pharma giant Pfizer was founded in 1849 by two German immigrants, initially as a chemicals business. However, when the American Civil War began, Pfizer saw huge demand for painkillers and antiseptics, and setting off the company’s transition to pharmaceuticals [9].

Interestingly enough, Pfizer’s involvement in the war would lead to the birth of another pharma giant. Colonel Eli Lilly, a cavalry commander serving for the Union, was also a trained pharmaceutical chemist who, after the war, set up his own pharmaceutical business in 1876. His company, Eli Lilly, would be one of the first pharma to focus on both R&D and manufacturing during a period in which early pharma focused on only one of the two [9].

1897 marked a breakthrough year for the pharmaceutical industry with the invention and commercialization of aspirin by the German company Bayer. Aspirin was one of the most successful drugs of its time and is still widely used today. However, in the aftermath of World War I, Bayer would have its aspirin trademark and U.S. assets seized while the American arm of Merck split off from its German parent company. These events would help propel the U.S. to the forefront of the industry while simultaneously setting back Germany for years to come [9].

Between the First and Second World Wars, arguably two of the most important pharmaceutical breakthroughs occurred: the discovery of insulin by Frederick Banting and colleagues in 1921 and the discovery of penicillin by Alexander Fleming in 1928. During World War II, an international effort between Merck, Pfizer, and Squibb mass-produced penicillin, saving thousands of lives. Furthermore, the scale at which penicillin was researched and manufactured set a precedent for how future drugs would be developed [9].

Post-war, the pharmaceutical industry entered a period of increase government involvement. With the arrival of healthcare systems such as the National Health Service in the U.K. that facilitated drug purchases and the National Institutes of Health in the U.S. that provided millions in R&D funding, pharma was booming in the late 20th century. Not only was pharma saving millions of lives, it was generating millions more in profit. In 1950, President of American Merck George Merck gave a warning about the purpose of the pharmaceutical industry: "We try never to forget that medicine is for the people. It is not for the profits. The profits follow, and if we have remembered that, they have never failed to appear. The better we remember it, the larger they have been" [9].

The latter half of the 20th century would mark the beginning of a period of rapid development and innovation. The 1970s were highlighted by the birth of the first “blockbuster” drug, Tagamet, an ulcer medication that drew in over $1bn in revenue in a year. The success of Tagamet ushered in the blockbuster model (explained later), which most big pharma companies still use today [9].

The 2010s ushered in a new era of pharmaceutical advancements due to rapid parallel developments in science. With the completion of the human genome project in 2003, pharmaceutical companies have been focusing on genetic-based treatments as well as immunotherapies, which do not directly act against the disease, but support the immune system in defeating the illness [9].

This ultimately leads us to the modern pharmaceutical industry. Now that we have a basic understanding of its origins, we can begin to understand the modern pharma landscape.

Pharma Business Model

Definitions and Classification

By definition, the pharmaceutical industry is comprised of companies engaged in the research and development, manufacture, and distribution of drugs. These drugs are intended for use in the diagnosis, cure, mitigation, treatment, and prevention of illness and disease. Within the industry, there are few key subsectors that emerge [2]:

Innovative/original pharma: Innovative pharma focuses on the development of novel, chemically synthesized drugs that are protected by exclusive marketing or patents. These companies invest heavily in R&D in order to discover new drug solutions. Examples include Pfizer and Roche [2].

Generic pharma: Generic pharma focuses on the production of generics, which are chemically equivalent copies of name-brand drugs. Generics can only be produced after patent expiration. Examples include Teva and Viatris [2].

Biopharma: Biopharma specializes in the production of biologics, which are drug treatments derived from living organisms. They are the biological counterparts of innovative pharma. Examples include Eli Lilly and Novo Nordisk [2].

Biosimilar pharma: Biosimilars are the generics of biologics. Biosimilar pharma is the biological counterpart of generic pharma. Examples include Catalent and Amgen [2].

Over-the-counter (OTC) pharma: While specialization in OTC medicines is rare, OTC pharma focus on the production of OTC drugs, which do not require a prescription to be purchased and used by consumers [2].

Do note that some of the companies listed as examples are not limited to their classification. Most, if not all, top pharma are widely diversified, meaning they have business lines in most of the above classifications. Furthermore, the distinction between innovative pharma and biosimilar pharma is minimal, and most top pharma can be classified as either.

Business Model

In our discussion of business models found in pharma, we will be focusing on innovative pharma. This is because a) the world’s largest and most influential pharma all have a very successful innovative pharma arm, and b) innovative pharma is the most unique type of pharma business due to the simple fact that there is no guarantee of a viable product.

Most modern pharma have adopted the “blockbuster” model. Statistically, only 10% of drugs that enter clinical trials ever make it to market. Of those drugs, the average return on invested capital (ROIC) is approximately 5%. However, blockbuster drugs, which are highly successful drugs due to their efficacy, can yield returns 10-20x as large as the average drug. Some of the most successful blockbuster drugs in history include Pfizer’s Lipitor with $164bn lifetime sales, AbbVie’s Humira with $137bn lifetime sales, and GlaxoKlineSmith’s Advair with $104bn lifetime sales. With the average cost of developing a new drug sitting at around the $1bn to $5bn range, each of these drugs generated handsome returns for their developers. Therefore, big pharma pours hundreds of billions of dollars annually into R&D in hopes of finding the next big breakthrough [5] [6] [14].

A quote from the Acquired podcast sums the pharmaceutical industry up perfectly: “Pharma is the most classic example of the venture business. It's super high risk, it's super high return if it works, and the winners need to subsidize all the failures”. In fact, approximately 10% of drugs that make it to market provide 50% of the profits in pharma, and most drugs do not even earn back their R&D costs, even after FDA approval [5].

Clinical Trial Process

We can now observe that the main attributes that make the pharmaceutical industry so unique are its high R&D costs and dangerous vulnerability to idiosyncratic risk. High R&D costs are inevitable for pharma, primarily due to the blockbuster model. Of the top twenty largest pharma in the world, the average R&D spend as a percentage of revenue is around 20%. However, recalling that only 10% of drugs that enter clinical trials are approved, pharma is highly susceptible to product failure. This is because all drugs must undergo the FDA’s rigorous, multi-phase clinical trial process, which is outlined below [5] [6] [16]:

Phase 0: This stage involves a very small number of people, usually fewer than fifteen, receiving a small dose of the medication. The purpose of this stage is to ensure that the medication is not harmful to humans in small doses.

Phase 1: This stage involves months of monitoring the effects of varying dosages of the medication on a larger group of people, usually twenty to eighty, who have no underlying health conditions. The purpose of this stage is to determine a safe dosage limit, and the optimal dosage method (orally, intravenously, topically), and determine some of the potential side effects. 70% of drugs make it past Phase 1 trials.

Phase 2: Phase 2 trials involve testing the medication on a few hundred participants who have the condition that the new medication is meant to treat. These participants are given the safe dosage determined in Phase 1 and the results are used to determine a general understanding of the efficacy of the medication and, if necessary, methods for testing in Phase 3. 33% of drugs (from Phase 1) make it past Phase 2 trials.

Phase 3: Phase 3 trials involve testing the medication on several hundred up to three thousand participants who have the target condition. Investigators must be able to show, with statistical significance, that the new medication is at least as effective as current treatment options. These trials are typically double-blind, meaning neither the investigator nor the participants know if they are receiving the treatment or a placebo. Since these trials often run for many years, they provide a better understanding of the potential long-term side effects of the new medication. Approximately 25-30% of drugs (from Phase 2) make it past Phase 3 trials.

After making it past Phase 3, the medication is submitted to the FDA for final approval. Therefore, even if a potential drug passes the gauntlet of clinical testing, it is still at risk of being denied approval by the FDA. While this is less likely, given the novel drug approval rate of 76% in 2022, it is still possible that years of research and millions in funding can be destroyed by an FDA decision. Post-approval, Phase 4 clinical trials take place, which are similar to Phase 3 trials in number of participants in length. These trials are meant to gather more information about the medication and its long-term effects [5] [6] [15].

Other Industry Trends

M&A is also an important part of big pharma strategy. A major theme in the industry is large-cap pharma acquiring small to midsize biotech companies with promising new drug solutions. These large-cap pharma are aiming to 1) fill pipeline gaps in the face of patent expirations and 2) acquire ownership of drugs that they see blockbuster potential in. The widespread implementation of aggressive roll-up strategies has enabled the industry to largely remain a conglomerate of diversified monopolies. However, large-cap pharma are also turning towards temporary partnerships as a way to meet consumer demand. Examples include the Pfizer and BioNTech partnership to develop the COVID-19 vaccine, or the Merck and Moderna partnership to create a cancer vaccine. Partnerships are also a way to skirt the antitrust concerns that are often raised during roll-up campaigns [1] [7] [13].

Recently, big pharma has been transitioning from the development of mass population drugs to specialty drugs that treat rare diseases. Since most common illnesses already have cures or adequate treatments, it is no longer financially viable to develop better treatments. Additionally, it is much harder to gain FDA approval for a drug if there already exists alternative treatments for the same disease. Comparatively, many rare diseases do not have existing or effective treatments, thus creating an opportunity for profit. Big pharma targets an underserved market, develops an effective solution, and then exercises unregulated pricing power to capitalize on the inelastic demand for their novel treatment. Since the pharma owns the only treatment available in the market, patients are forced to oblige with the high prices. Pharma’s pricing strategies have been an area of major controversy for the past decade, which we will explore in a later section [1] [5].

Market Landscape

Industry Overview

The modern pharmaceutical industry is characterized by the dominance of a handful of large corporations, nicknamed “big pharma”. These corporations are located primarily in the United States and Western Europe and control a majority of the pharma market [1].

2023 was a year of change at the top for pharma. Danish pharma Novo Nordisk, known for its insulin solutions, made a significant leap in the revenue rankings, from seventeenth to twelveth, thanks to the success of its weight loss drugs Ozempic and Wegovy. Similarly, American pharma Eli Lilly also saw impressive revenue growth, benefitting from its own weight loss drugs Mounjaro and Zepbound [3].

2022 revenue leader Pfizer, however, took a major hit after COVID-19 vaccine demand drastically fell off in 2023. After recording an industry record of $100bn in revenue in 2022, Pfizer’s revenue fell by 42% to $59bn in the following year. Pfizer’s fall from the top enabled Johnson & Johnson to regain the top spot with its revenues growing 6.5% Y/Y to $85bn. COVID vaccine manufacturers Moderna and BioNTech fell out of the top twenty highest-earning pharma, also due to the decline in COVID-19 vaccine demand, with generic pharma Teva and Viatris replacing them [3].

Market Performance

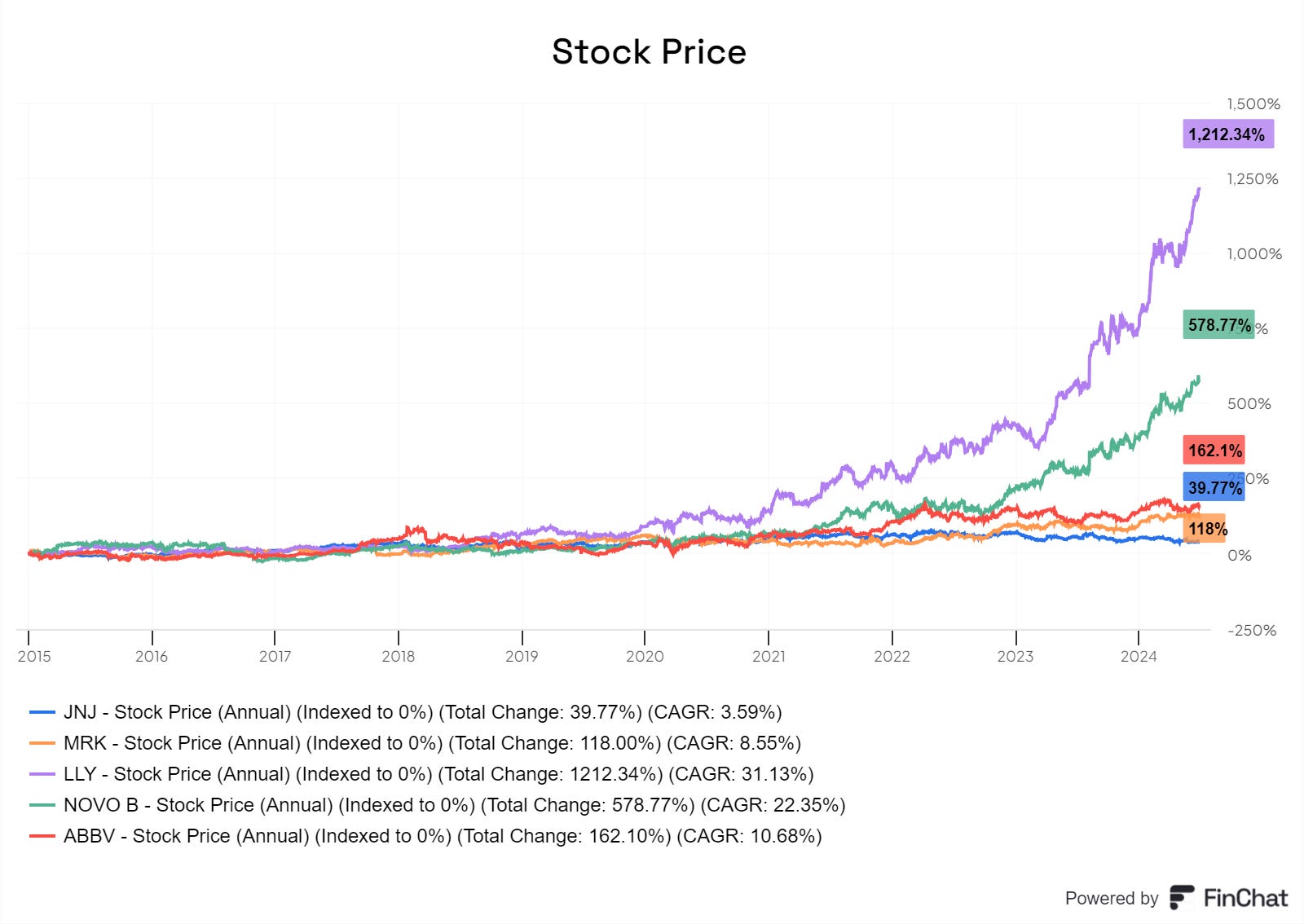

As of September 2024, the top five largest pharmaceutical companies in the world by market cap are Eli Lilly (American), Novo Nordisk (Danish), Johnson & Johnson (American), Merck (American), and AbbVie (American). In the context of the broader economy, Eli Lilly’s $840bn market cap makes it the tenth largest company in the world by market cap. Merck, at $290bn, is ranked thirty-third in the world [11] [12]. See here for these stock performances over the last decade.

The past decade has been a period of slow revenue growth generally speaking. Johnson & Johnson’s ten-year revenue CAGR was only at 2%, Pfizer was at 1%, and Merck was at 3%. Additionally, operating income growth has been even weaker: Johnson & Johnson’s ten-year operating income CAGR was at 3%, Pfizer at -5%, and Merck at -3%. However, these poor growth rates are not as much a result of industry-wide downturns but more a result of company-specific causes [20].

The same trend of slowing revenue growth does not apply to Eli Lilly and Novo Nordisk. As expected, these two companies were the main beneficiaries of the weight loss drug craze, with Novo Nordisk’s market cap more than quintupling since 2020, from around $100bn to over $590bn [3].

The industry as a whole still remains highly profitable, especially for big pharma. As of 2024, Johnson & Johnson, Roche (Swiss multinational healthcare titan), and Merck boasted operating margins of 23%, 26%, and 28% respectively, well above the industry average of ~15%. For context, Apple’s operating margin in 2023 was 26%, indicating that the top pharma companies are highly profitable, even matching the performance of big tech [20].

Valuation

The valuation of pharma companies often differs from traditional companies due to the high-growth, high-profit, and high-risk nature of the business. Additionally, many early-stage pharma companies post years of consecutive, negative revenue and high cash spend due to their immense R&D costs, which may not reflect the true value in the company, such as in the case that they have a potential breakthrough drug in development.

The commonly used approaches are net present value (NPV) analysis, risk-adjusted NPV (rNPV) analysis, real options, comparable trading analysis, and precedent transactions analysis. Each of these methods may be used to valuate pharma companies, depending on the specific context of each company [17] [18].

Net present value analysis: An NPV analysis usually involves the use of a discounted cash flow (DCF) based method. A DCF analysis utilizes a company’s present and future cash flows to estimate the present value of the business. However, an NPV analysis is only suitable for established pharma who generate yearly, stable cash flows.

Risk-adjusted NPV analysis: A risk-adjusted NPV analysis is similar to an NPV analysis but it also takes into account factors such as the probability of success of the company’s products. For pharma companies, this means a risk-adjusted analysis factors in the probability of their research or clinical trials being successful into the valuation. This approach often offers a more accurate valuation for pharma companies.

Real options: Real options is a more technical method of valuation that treats business investments like “options” instead of static projects. Real options aims to quantify the tactical decisions that executives can make, which are not usually factored into traditional valuations. For pharma and biotech startups, every decision the management team makes holds some type of value, whether that’s expanding successful trials into additional uses, ending failed trials to save cash, or securing new patents. Each of these decisions, or “options”, represents an intangible value that real options aims to factor into valuations. In other words, companies can make investments that give them an option, but not an obligation, to capitalize on future opportunities.

Comparable trading analysis: Comparable trading analysis, or comps, is a method in which a company is valued based on the similar companies whose valuations are known. This type of approach is often used when a pharma company is preparing for an initial public offering (IPO), so it is compared to public- traded companies to determine its true value.

Precedent transactions analysis: Similar to comps, precedent transactions analysis is a method that compares the pharma business to similar companies. However, instead of comparing company to company, this approach uses the M&A transactions of similar companies to valuate the target company. Precedent transactions is also very important when it comes to determining an appropriate acquisition price for a pharma company because the acquirer can use historical data to determine the correct price to pay.

Financial multiples are also important in determining the health, performance, and value of a pharma company. Traditional multiples such as EV/EBITDA and P/E can be used for established pharma companies, such as Johnson & Johnson and Merck. For context, in 2023, the average EV/EBITDA multiple for traditional pharma was 13x, which is in line with biotechs (trading at 13x as well). However, for pharma that have not yet begun to generate consistent EBITDA or earnings, some investors opt for the forward P/E ratio, which uses forecasted earnings to calculate P/E. This accounts for the future potential earnings that many early-stage pharma have [17] [18] [19].

Over the past few years, valuations of pharma and biotech startups have fallen dramatically. Between 2018 and 2021, the average fully diluted valuation of biotech companies going public was $827mm. However, in 2022, that number fell to just $123mm. In 2023, the average funding raised by biotech IPOs was approximately $140mm. This decline in valuation and funding indicates that investors are no longer willing to pour their money into any biotech with some kind of potential [18].

Controversies and Criticisms

Pricing Scandals

The pharmaceutical industry has faced harsh criticism and countless controversies throughout the years. One of the more recent incidents occurred in 2015, when then-CEO Martin Shkreli of Turing Pharmaceuticals raised the price of Daraprim, a drug used to treat malaria and certain HIV/AIDs complications, by 5000%, from $13.50 to $750. Shkreli was quickly dubbed “the most hated man in America”, however, his actions were completely legal. Since then, Daraprim’s price has yet to return to its original price, and the incident clearly highlighted major flaws within the pricing schema of the pharmaceutical industry [1].

Another example of a pharmaceutical pricing controversy occurred in 2014 when American pharma Gilead launched Sovaldi, a highly effective drug that cured hepatitis C in three months of use. Its launch price was $84,000 for three months, or $1000 per tablet. Interestingly, Gilead had minimal involvement in the production of Sovaldi, which was primarily developed by university researchers and a small biotech firm named Pharmasset but was able to charge an astronomically high price after gaining ownership. Leaked Gilead marketing documents indicated that public health concerns were never a consideration in the pricing of Sovaldi, further sparking public outrage. Significant price reductions for Sovaldi were able to be established by the development of generics on the guarantee that cheaper generics would open up new global markets, but this generic was solely available in developing countries. Patients in countries such as the U.S. and Europe would still be forced to pay however much Gilead charged [1].

Another major scandal involves the drugs Avastin and Lucentis and pharma Novartis and Roche. Avastin was first launched in 2004 by Genentech as a drug designed to treat colon cancer. However, an American professor would discover that Avastin also had eyesight-improving properties and, importantly, delayed the development of a disease known as age-related macular degeneration (AMD), a degenerative eye disorder that often led to blindness or partial blindness in older people. With the discovery, Genentech began developing a new drug based on Avastin that was purposed solely to treat AMD. When Lucentis was ultimately launched, it cost about $2000 per dose compared to Avastin at $50. Naturally, hospitals and clinics favored the cheaper alternative, although it was not officially purposed to be used for AMD. In an effort to sell its product, Novartis, which owned Lucentis at the time, sent out representatives to hospitals urging them to switch to Lucentis. Furthermore, along with Roche, which owned Avastin (and Genentech), Novartis began extensive lobbying campaigns in France to force hospitals to transition to using Lucentis. The lobbying was ultimately successful, forcing hospitals to purchase the more expensive option. However, after an investigation by French authorities years later, Novartis and Roche would be fined hundreds of millions for the illegal price fixing of Lucentis. Coincidentally, Novartis owned one-third of Roche at the time [1].

Reform

Pricing remains big pharma’s most controversial issue and reform is long overdue. As of 2023, one in four Americans cannot afford their prescribed medications, and “retail prescription drug spending, on a per-capita basis, has almost quadrupled since 1990, increasing from $266 to $1025” [4] [10].

Big pharma’s immense pricing power stems from the broken pharma patent system. Pharmaceutical companies abuse the patent system by securing new patents for insignificant changes to their drugs (such as how the drug is flavored) in order to extend their pricing monopoly on the drug. Instead of investing time and resources into developing newer, better treatments, big pharma often prioritizes extending the patent lifespan of older drugs. Each extra day a blockbuster drug is under patent protection generates tens of millions in sales [4].

Outlined below are five key steps towards reforming the pharma pricing system, per the Initiative for Medicines, Access & Knowledge (I-MAK) and Patients for Affordable Drugs, two non-profit organizations focused on public health and pharmaceutical reform:

Price negotiations: Allowing Medicare and other insurance providers to negotiate prices of high-cost drugs will decrease the pricing power of big pharma and bring regulation into the system [4].

Patent reform: Reforming the patent system by raising the bar for what can and cannot be patented through cooperation between Congress, the FDA, and the Patent and Trademark Office (USPTO) will ensure that big pharma cannot obtain obscenely long patent periods for arbitrary reasons [4].

Develop transparency: Developing transparency within the USPTO to ensure that big pharma does not receive patents due to the secondary interests of PTO officials will prevent pharma companies from benefiting from bribery and corruption [4].

Simplifying patent challenges: Reforming the patent challenging process by decreasing its cost and simplifying it will allow the broader public to contest the unjust patents of big pharma [4].

Government involvement: The federal government can implement taxes and fines against price-spiking pharma, punishing them for doing so and blocking future attempts [10].

While this list is not exhaustive, it outlines key objectives that reformers should aim to achieve in order to create a pharmaceutical pricing system that prioritizes public health and wellbeing over corporate profits.

Contemplating the Future

With the rapid advancement of science and technology in the 21st century, innovation in the pharmaceutical industry will only continue to accelerate. Let’s examine a few of the key considerations influencing the future of big pharma:

AI and analytics: AI will likely play a pivotal role in the innovation of almost all industries, pharma included. Big pharma is already looking towards accelerating growth through the incorporation of AI and analytics into their business models. According to a PwC analysis, AI-enabled automation within pharma business models is projected to create a 60-70% reduction in drug process timelines, a reduced burden for patients, providers, and related companies, and a 30% reduction in operational costs. Furthermore, a PwC survey stated that 89% of pharma companies were planning on increasing their technology budget over the next twelve months. The potential of AI is unparalleled, and pharma companies must take full advantage [8].

New healthcare technologies: With science and tech evolving faster than ever, new research and advancements in healthcare are being developed every day. Treatments involving new genetic tools such as CRISPR-Cas9 and other biotech solutions will soon become integral parts of big pharma portfolios. Furthermore, the implementation of AI in the process of identifying viable chemical compounds for pharmaceutical purposes will further accelerate the drug development pipeline [8].

Increased collaboration: Collaboration between pharma, governments, and healthcare providers will likely increase over the next decade. With many large-cap pharma already taking part in partnerships, this type of cooperation will only increase [8].

Sources: [1], [2], [3], [4], [5], [6], [7], [8], [9], [10], [11], [12], [13], [14], [15], [16], [17], [18], [19] [20]

Upcoming Free Educational Events from Leland

Sept 17 - Breaking Into Investment Banking Panel

Sept 26 - Private Equity 101 (Highly Recommend)

Interested in our updated reading / wellness list? Check it out here.

How did you like this week’s Pari Passu? Loved | Great | Good | Meh | Bad

Interested in our IB / PE / Finance course recommendation? Check it out here.

Looking for more Pari Passu Content? Check out Instagram | Twitter | Linkedln