Triple Dip Primer and Spirit Analysis

Triple Dip Primer and Spirit Analysis

Welcome to the 92nd Pari Passu Newsletter,

Three weeks ago, we looked into a hot iteration of Liability Management Transactions: double-dips. As a reminder, this is a mechanic created naturally in capital structures over a decade ago made two claims for a single creditor group, effectively doubling their recoveries.

Over the past few years, we have seen double-dips emerge as a new form of transaction where creditors are now actively implementing verbiage in credit documents as a restructuring solution. These two claims typically come from intercompany loans and guarantees from the parent company or restricted guarantor subsidiaries.

However, recently, a proposal from the bondholders in Spirit Airlines (NYSE: SAVE) introduces a new concept: triple-dips. In this paper, we will first understand how triple-dips could be created. Then, we will analyze the real world case of Spirit Airlines and see the potential of the triple-dip as a revolutionary liability management maneuver.

But first, a message from 10 East

10 East, led by Michael Leffell, allows qualified individuals to invest alongside private market veterans in vetted deals across private credit, real estate, niche venture/private equity, and other one-off investments that aren’t typically available through traditional channels.

Benefits of 10 East membership include:

Flexibility – members have full discretion over whether to invest on an offering-by-offering basis.

Alignment – principals commit material personal capital to every offering.

Institutional resources – a dedicated investment team that sources, monitors, and diligences each offering.

10 East is where founders, executives, and portfolio managers from industry-leading firms diversify their personal portfolios.

There are no upfront costs or minimum commitments associated with joining 10 East..

Double-Dip Overview

Let’s get to it. Triple-dips are simply an extension of the double-dip transaction, so it is critical to understand the mechanics of the double-dip first. Simply put, a double dip transaction is when new financing is provided such that the lender is entitled to receive, at most, two times of their book value of debt provided. How we get to two claims comes from two sources: an intercompany loan and a guarantee from a parent/restricted entities. An intercompany loan is a lending agreement between two entities in the same corporate structure (hence the ‘inter’). Specifically, it occurs when one entity, let’s say Subsidiary X, lends capital or assets to Subsidiary/Parent Y. Because the capital has been lent, Subsidiary/Parent Y is indebted to Subsidiary X.

A guarantee is when one party provides an ‘assurance’ to another party in the same corporate structure. One of the key rules surrounding investing in debt across the capital structure is that lenders want to lend as close to where the true value of the company resides. Ideally, this means that lenders provide capital to the entity that holds the valuable assets of the entire company. Thus, the point of a guarantee is to ensure that claims that are held at different lengths from the key assets are treated pari passu rather than one claim being structurally subordinated to another claim.

To explain this example further, let’s look at a waterfall with and without a guarantee. Let’s say that we have a capital structure consisting of ParentCo debt of $400mm and SubCo debt of $400mm. Additionally, we know that the assets, totaling $500mm, reside at the ParentCo. Because the ParentCo debt sits ‘closest’ to the assets, they have the first claim. Thus, in a situation without a guarantee, the ParentCo debt would receive 100 cents while the SubCo debt would receive 25 cents. However, with a guarantee extended from ParentCo to SubCo, the debt is now treated pari passu. Thus, the recoveries are now both 62.5 cents for both tranches of debt. This can be seen in Figure 1.

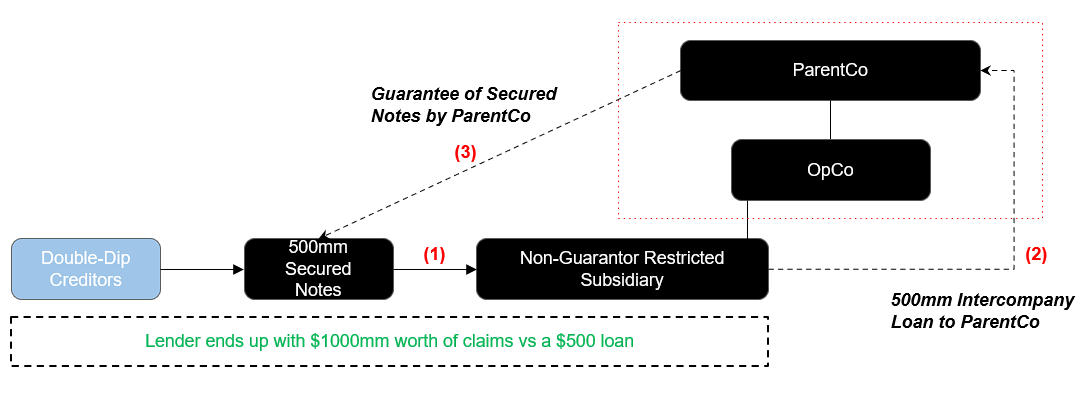

Now, we can apply this knowledge to visually demonstrate how double-dips are created. As seen in Figure 2, the double-dip has 3 components.

An entity lends money to an empty box (the non-guarantor sub).

This box then transfers that money (in the form of an intercompany loan) to another box (the restricted sub or ParentCo) with pre-existing debt / assets.

The ParentCo then guarantees the initial loan (pari to pre-existing debt), creating a second secured claim for the double-dip creditor . This creates two claims from one initial loan, thereby resulting in a double dip structure.

There are two important points to note: First, both the intercompany loan and guarantee can provide a recovery of at most par. This means that if the intercompany loan does not recover par, the guarantee cannot return above par such that the creditor can still receive two times recovery. Additionally, the reason we are saying, ‘under perfect conditions’, is because in reality it is very unlikely that double dip creditors receive two times their claim. Double-dips only provide value in a bankruptcy situation (either for liquidation or negotiating power in terms of what the true value of a claim is), and because the company is in bankruptcy, it is unlikely that it has the capital to return par to its creditors. Additionally, double-dips are heavily restricted by their credit docs. For example, oftentimes there is a guarantee cap in credit docs. This limits the amount of debt that an OpCo can guarantee, leading to a slightly below double recovery [13].

Triple Dips

A structure that is just arising, however, is the triple-dip. The point of a triple-dip is simply to take a double dip, and determine if there is another claim that can allow a creditors claim to reach three times the book value of debt. The case of Spirit Airlines, which we will dive into later, is the first iteration of this mechanic and evidence that triple-dips can be created if the correct verbiage exists in credit documents. For Spirit, a third dip was created via Termination Damages, as the bond indenture included a clause specifying the cost of damages owed to bondholders if the brand IP licensing agreement is terminated. The other two dips came from the sources above: the ParentCo guarantee and an intercompany loan. However, the Spirit triple-dip is currently being subject to scrutiny and claims that the damage dip is not as strong as the bondholders initially claimed. That does pose the question: what are some other ways a triple-dip could be created. Although it is always going to depend on the credit doc, corporate structure, and what creditors are allowed to do, below are some possible ways that we have thought a triple-dip could be created. Note: these are just our thoughts, and by no means the ‘correct’ way to go about the triple-dip maneuver. In the end, a triple-dip will require large flexibility from the credit docs, and there could be endless ways for it to be structured.

Option 1: Subsidiary Structuring

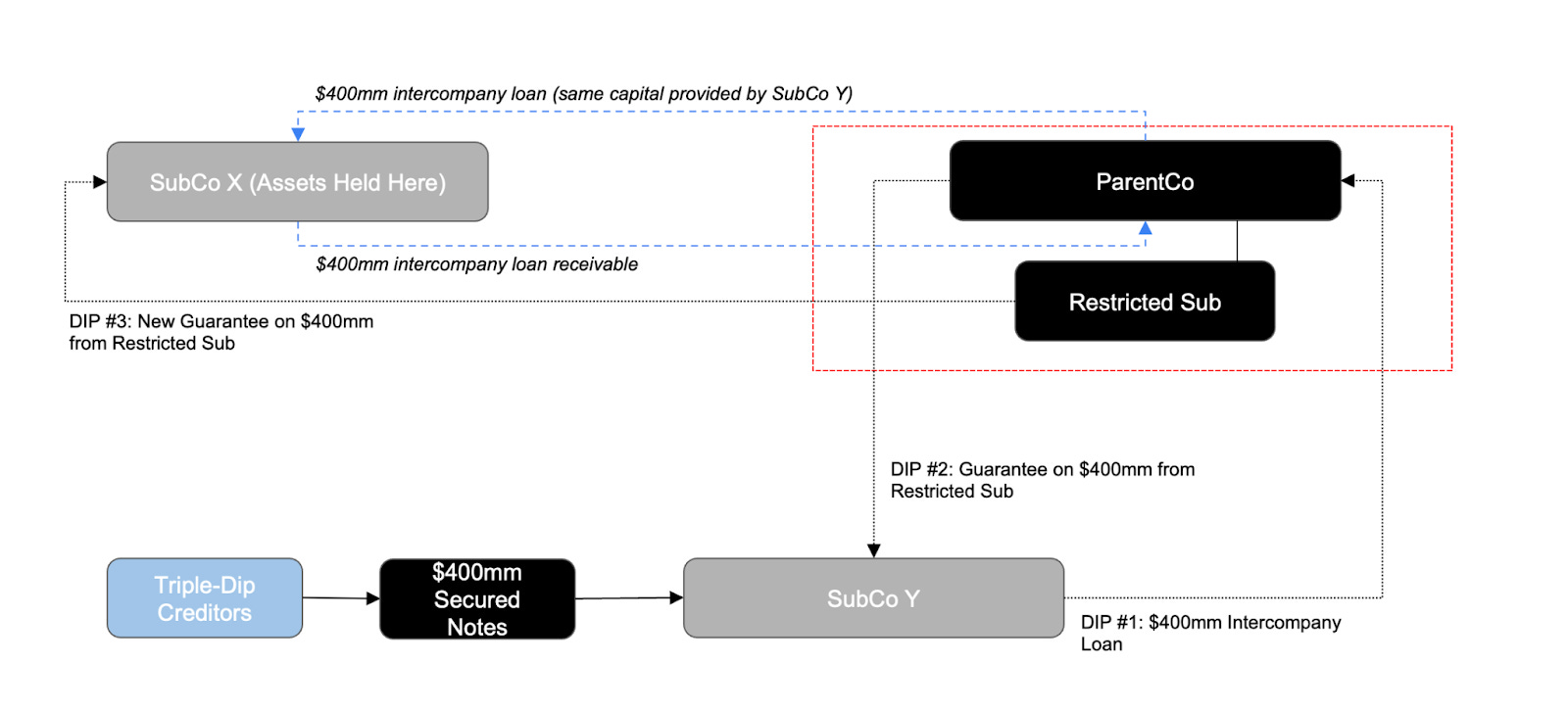

This version of a triple-dip is going to be the most dependent on the credit docs, but can be thought of as the most natural extension of a double-dip. In a double-dip, we gain two claims from an intercompany loan and a guarantee. Although it may seem simple to create a new subsidiary and provide another intercompany loan, for example, to get a third claim, this would not actually provide a triple-dip as this new intercompany loan still requires capital from a creditor group. Thus, to create a triple-dip ‘naturally’, we need to maneuver the existing capital around the corporate structure to gain an additional guarantee secured by the same pool of assets. Reference Figure 3 below for an example to demonstrate this idea.

While this diagram may look complicated, it is simply an extension of the double-dip seen in Figure #2. In this example, we have $400mm of Secured Notes being issued to SubCo Y. As in a standard double-dip, we have our first claim coming from an intercompany loan to the ParentCo. Our second dip comes from the guarantee from the restricted subsidiary on the $400mm debt issued by the triple-dip creditors. Now, to create the third dip, we need to gain an additional claim. To do so, one method could be to transfer the debt held at ParentCo to SubCo X via an intercompany loan. The debt held at SubCo X can then be guaranteed again by the Restricted Sub, creating a third claim. In order to move assets in and out of the credit box like the example above, there needs to be a lot of credit doc flexibility.

Option 2: Intercompany Derivative/Capital Structure Instruments Structuring

A company could use swaps, options, and other derivative instruments between subsidiaries to create a third claim. Like the intercompany loan, a derivative instrument represents a contract between two parties, and if structured appropriately, it could represent additional recoveries for the triple-dip lenders.

Figure #4 depicts how this structure could arise. As it was in Figure #3, there is a first claim from the $400mm intercompany loan, and a second claim from the $400mm restricted company guarantee. However, the third claim is created via an interest swap contract entered into between SubCo X and ParentCo (using the $400mm upstreamed from SubCo Y). To briefly explain how swap contracts work, it is an agreement between two parties to exchange their interest payments for one another over a set period of time. Let’s say that we have a mortgage of $1,000,000, with a 10% fixed interest rate. If we believe that interest rates are going to be lower than this rate over the duration of a swap contract, an individual can engage in a swap contract with a bank. To do so, they would swap their 10% fixed interest rate for a rate that the bank provides, say SOFR + 2%. If the contract lasted 5 years, each year the bank would have to pay the 10% rate and the individual would only have to pay the SOFR + 2%.

In our example swap contract, we can assume that it has a notional value of $400mm, where SubCo2 pays a fixed rate (i.e 5%), and ParentCo pays a floating rate (i.e SOFR+3%). If, at the time of the filing, the present value of the swap contract is positive to the benefit of SubCo X, it becomes an additional claim. Thus, if that swap contract reached a present value of $400mm, a third claim could be created.

There are a few conditions for the swap contract to occur. First, getting the ParentCo to engage in an intercompany swap contract would undoubtedly be difficult, as they are not common within a corporate structure. Additionally, the credit docs would have to be loose enough, perhaps looser than the 2020-2021 ‘cov-lite- era, to allow 2 Subs to be created.

Option 3: Contingent Convertible Capital Securities

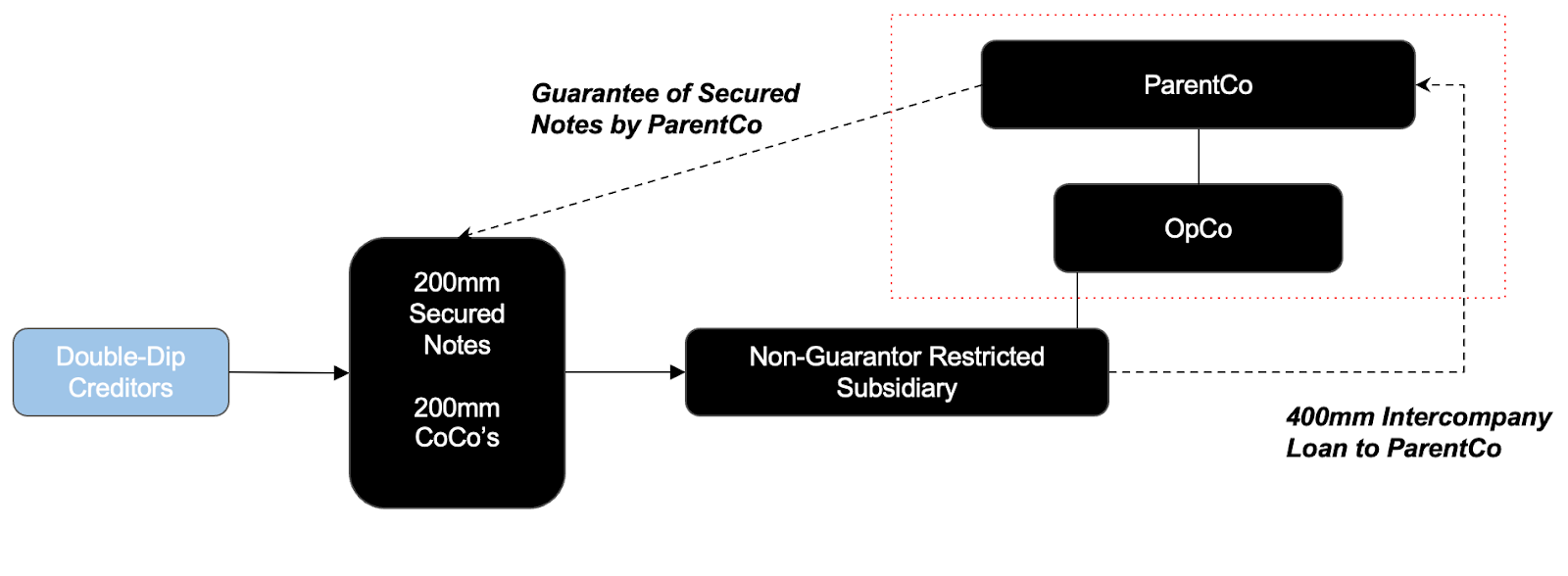

Additionally, a triple-dip could be created via another capital structure instrument such as Contingent Convertible Capital Securities (CoCos). Contingent convertible capital instruments are hybrid securities that can absorb the losses of financial institutions. These instruments can be written off to zero or converted to equity. The primary purpose of these securities is to assist banks in distress. CoCos are structured to absorb losses even to the point of bankruptcy. However, these securities don't always act as a loss-absorber. They have to be 'activated.' They can either activate mechanically by breaching a specific covenant or activated via the discretionary judgment of a financial regulator.

In the case of CoCos, let’s take a standard double-dip situation and add 1 layer of complexity - this can be seen below in Figure 5. However, let’s now assume that of the $400mm of capital provided to SubCo Y, $200mm come from Secured Notes while the other $200mm are Contingent Convertible Capital Securities. We would still gain two claims from upstreaming $400mm as an intercompany loan and getting a guarantee on the $400mm of debt issued. However, the CoCos could provide additional value if certain situations occur. Once our company files for bankruptcy, the trigger will most likely have been activated with two outcomes: either the $200mm has been converted to equity or written off completely. Although it may make sense from the company perspective to write off the debt as they are likely to be impaired under distress, this may not be feasible. The reason for this is because of recent litigation involving the Credit Suisse case. Although our current case is hypothetical, the evolving nature of the CoCos market is not. In the Credit Suisse case, the CoCos were written off, which consequently led to heavy litigation that ultimately cost the company more than the CoCos were actually worth. Thus, companies in the future may be more inclined to treat CoCos as equity if given the choice via a mechanical trigger. In that case, the triple-dip creditors now have a valid claim in bankruptcy courts, and like many recoveries, their return is heavily dependent on valuation fights. Our hypothetical triple-dip creditors could navigate a value fight such that they create a valuation high enough that gives equity some recovery. Because equity has unlimited upside, this triple-dip is not ‘conventional’, but in the long-term could provide over three times recoveries for these creditors.

There are a few requirements for CoCo triple-dips to occur as well. First, CoCos are typically used for financial institutions, so finding value leakage and winning value fights in these cases are very difficult. Additionally, this example is highly variable and recoveries are uncertain. However, all of these examples provide a method to capitalize on distinct, capital structure situations. As it was back in 2008/2009, the double-dip was not sought out in the Lehman Brothers bankruptcy, but rather existed naturally and was capitalized on by aggressive creditors seeking improved recoveries.

Why are Triple Dips created?

You might be asking yourself: what is the point of this? Admittedly, at a first glance this entire structure seems counterintuitive - there are a variety of ways for a distressed company to raise capital - many of which don’t require the capital / asset structure to be organized in such a large manner.

From our point of view, there are two reasons for why this is happening. The more ‘obvious’ one is the result of a last ditch effort. Companies that are truly on the borderline of distress - where cash burn is so large that a company has a few months, if not a few weeks, before they breach their covenants. To come to an agreement with creditors in such a distressed situation requires high flexibility and many concessions from the debtor. To a creditor - the triple dip is the perfect structure. In theory, it offers a recovery of at most 3x their investment in the case of bankruptcy. If a company only has a short time frame before they run out of liquidity, a triple dip offers a strong cushion for creditors. In the case that the company does file, they are now in a prime position to generate a strong return. If the company manages to use a triple-dip creditor’s investment to successfully turn around the business, then the creditor would generate large returns from what was incredibly generous pricing and terms at the time of the loan.

The second reason for why this structure is occurring, in one word, can be boiled down to ‘evolution’. If we go back to the origin of the double-dip, it was never ‘intentionally’ made. The Lehman Brothers creditor’s noticed the terms when the company filed for bankruptcy, and took advantage of the situation. A decade later, double-dips are now intentionally used in advance of a bankruptcy for creditor protection. Triple-dips can be thought of in the same manner. As we will see in the Spirit case, the triple-dip created was unlikely thought of in advance, but rather the creditors noticing the situation within the credit docs. While it might not be a decade away, it is fair to assume that triple-dips may take that same evolutionary pattern, and be used as a form of creditor value preservation.

As we will see in the Spirit Situation, triple-dips are new and getting the third claim is going to be contested in and out of bankruptcy courts. However, eventually, it is plausible that a situation will occur where a creditor can seek three dips due to loose credit docs or unique capital structure situations.

Spirit Triple-DIP

All of the aforementioned examples are theoreticized, so let’s look at the real life example of Spirit and analyze how the triple-dip was actually created.

Company and Industry Background

Spirit Airlines' roots trace back to 1964 in Macomb County, Michigan, where it initially operated as 'Clippert Trucking Company'. 1977, the firm evolved into the Grand Air Transfer inch before switching into the aviation industry in 1983 as Charter One Airlines. As the commercial aviation space was booming in the late 1970s/'80s, Spirit aimed to capitalize on this growth as it became more affordable to the broader population. Their goal was simple: offer cheaper packages for those looking to travel to holiday destinations where entertainment was the key driver. Under Charter One Airlines, the company had flights to the Bahamas, Las Vegas, and Atlantic City. In the 1990s, the firm began to offer these cheaper flights to more cities, including Boston and Providence. In 1992, Charter One Airlines rebranded as Spirit Airlines and started to schedule nationwide routes [7].

However, as we have moved into the 21st century, Spirit has begun to struggle within space for various reasons, leading to the company's current distressed situation. However, the glaring issue for Spirit is the increased competition in the aviation industry and the fundamental flaws of the company's business model. Touching on the first point, Spirit has had to contend with various competitors. American Airlines, Delta Airlines, United Airlines, Jet Blue, and Hawaiian Airlines were founded in 1926, 1925, 1926, 1998, and 1929, respectively. Barring JetBlue, which has a solid competitive advantage in the space, Spirit's competitors have decades more experience and developed a loyal customer base, leading us to our second point: the fundamental flaws of the business model.

As aforementioned, Spirit's competitors have developed a loyal customer base. The question that Spirit asked themselves in 1992, which we should ask right now, is what drives a loyal customer base. Some might argue that it is the experience one has with an organization. However, taking that notion one step further, it is more likely how individuals remember their experiences with an organization. Even if you had a trip with an organization that completely deviated from their predetermined schedule and threw numerous surprises at you, if that deviated schedule was a positive experience, you would likely view that company positively and become a recurring customer. This gets to the core of why Spirit has not been able to be competitive as time has progressed. When the firm was created, their business model centered around a low-cost experience - this was the only way they could break into a space dominated by their peers. While this worked at initially attracting customers, it has not been a source of recurring revenue. While there will always be individuals whose primary travel goal is to obtain the cheapest experience, many often look for a ride with strong customer service, for example. Because of the 'low-cost' priority, Spirit has been unable to provide the same quality of food, entertainment, and overall experience, which hurts how people view the company and their prior travels.

The airline industry is also faced with numerous headwinds. First, the industry has considerable upfront costs. You must have many planes to run a successful airline company, often costing hundreds of millions of dollars. Furthermore, airline companies' margins are usually low due to bloated cost structures. Airlines need large labor forces to run their operations, from flight attendants to pilots, baggage handlers, etc. Labor is a significant source of cash burn for Spirit. Since the COVID pandemic, airlines have scrambled to find labor. In 2023, Spirit Airlines pilots agreed to a two-year contract with an average 34% wage increase [9].

Additionally, it is essential to note that only 61% of union members agreed to this increase. The union stated that the agreement was conditional under a JetBlue-Spirit merger occurring, and if the deal failed, the Spirit pilots would re-enter negotiations [9]. Oil volatility is another challenge that airlines have to deal with, as periods of rapid oil price increases can be burdensome. To fund all these costs, airlines take on lots of debt (typically collateralized by fixed assets), and these interest expenses further bite into airlines' net income. Spirit has been subject to all of these issues, putting them into a place of distress, as we are currently seeing.

Spirit Airlines M&A Timeline

Spirit's controversial M&A proposals began in early 2022, with a merger agreement established between Frontier Airlines and Spirit. The transaction was expected to close in the second half of 2022 and valued Spirit at an equity value of $2.9bn and a transaction value of $6.6bn. With Frontier being another ultra-low-cost carrier, the merger was based on the premise that these companies could combine highly complementary networks and increase access to ultra-low fares by enabling new routes in the United States. As cited in the investor presentation upon the merger announcement, the deal offered $500mm in operating synergies and the ability to offer $1bn in annual consumer savings. The combined entity was estimated to generate $11.9bn in revenues [11],[14]. This deal would have made Spirit/Frontier the fifth-largest airline operator in the country. However, on May 16, 2022, JetBlue launched a hostile takeover of Spirit Airlines, offering shareholders $30/share (and stated they were willing to pay $33/share if negotiations commenced shortly after that). This takeover came upon announcements that Spirit's shareholders were not convinced of the Frontier merger. Following this news, Frontier provided a sweetened deal, increasing the offer price by $2/share, stating this was their final deal. Despite these deals, Spirit's shareholders were unconvinced with the Frontier merger, and on July 27, 2024, the Frontier deal was terminated, and Spirit continued negotiations with JetBlue [10].

The JetBlue/Spirit merger agreement was signed on July 8, 2022. It was an all-cash transaction, with Spirit shareholders receiving $33.5/share in cash, a $2.5/share prepayment premium, and a $0.1/share monthly ticketing fee prepayment starting January 2023. A monthly ticketing fee prepayment refers to the additional payment made from JetBlue to Spirit. Spirit shareholders will receive a recurring payment of $0.1/share each month. This deal estimated $600-700mm in net annual synergies, driven by increased network relevance, schedule optimization, greater loyalty relevance, and economies of scale on an existing cost basis [11].

While the numbers seem strong and offered a substantial premium to Spirit's trading price pre-announcement, the offering had a fundamental flaw. JetBlue is a high-cost carrier, unlike Frontier/Spirit, where both companies were low-cost carriers. Thus, the JetBlue/Spirit merger would effectively eliminate competition in the Spirit market, violating antitrust laws. This happened to be the case, as in March 2023, the Department of Justice sued to block the merger, arguing that the deal would dampen innovation and reduce competition. The DOJ cited two main arguments:

The DOJ conducted an internal analysis and found that fares declined 16% when SpiritSpirit entered the market and increased 30% when SpiritSpirit exited. This demonstrates the deal's anti-competitive nature.

The DOJ cited Spirits' claims in 2022 about the harm to competition from a JetBlue Merger.

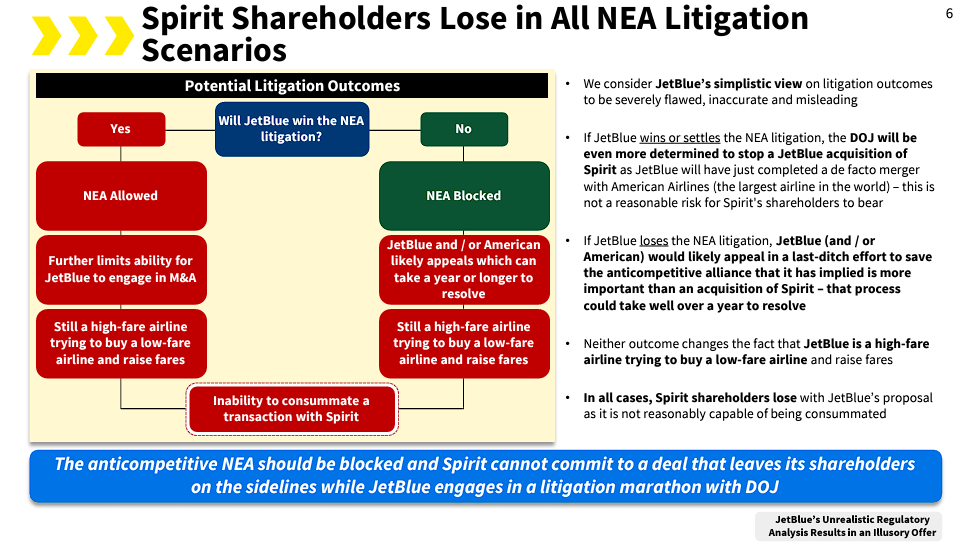

Further detail is needed to explain the second point. When JetBlue came in with their hostile takeover proposal, Spirit's board believed that the Frontier deal offered the best upside for shareholders and released an investor presentation contemplating why the JetBlue deal would not make sense. These reasons can be seen in Figure 5.

While many of these points are evident based on the description in the image above, the first bullet requires additional attention. The JetBlue offer is “illusory” and incapable of being consummated because JetBlue was involved in ongoing anticompetitive suits regarding the Northeast Alliance between JetBlue and American Airlines. Under the Northeast Alliance, JetBlue and American would jointly schedule flights and split revenue on their operations out of the Boston, Newark, LaGuardia, and JFK airports. The Massachusetts federal court found this alliance a clear violation of antitrust laws and prohibited this alliance from going through. Regardless of what happened in NEA litigation, Spirit shareholders were expected to lose in all scenarios (as depicted in Figure 6)

However, JetBlue abandoned the NEA proposal to focus on the Spirit acquisition once the Frontier deal fell through. To combat the DOJ and Spirit’s previous position that a JetBlue/Spirit deal would be anticompetitive, JetBlue and Spirit announced divestiture agreements. Namely, Spirit agreed to give their assets at Laguardia to Frontier and their holdings in Boston to Allegiant Air. JetBlue decided to give up five gates at Fort Lauderdale. The belief was that these were the company's critical assets that made this deal ‘anti-competitive,’ and the DOJ would allow the deal to go through by divesting it. However, the DOJ found that the divestitures were insufficient. Despite any efforts, any consolidation involving Spirit would be subject to antitrust litigation as Spirit is irreplaceable as the largest ultra-low-cost carrier. On March 4, 2024, the DOJ won the battle, and the Spirit/JetBlue merger was officially scrapped, stating there was no path forward [5].

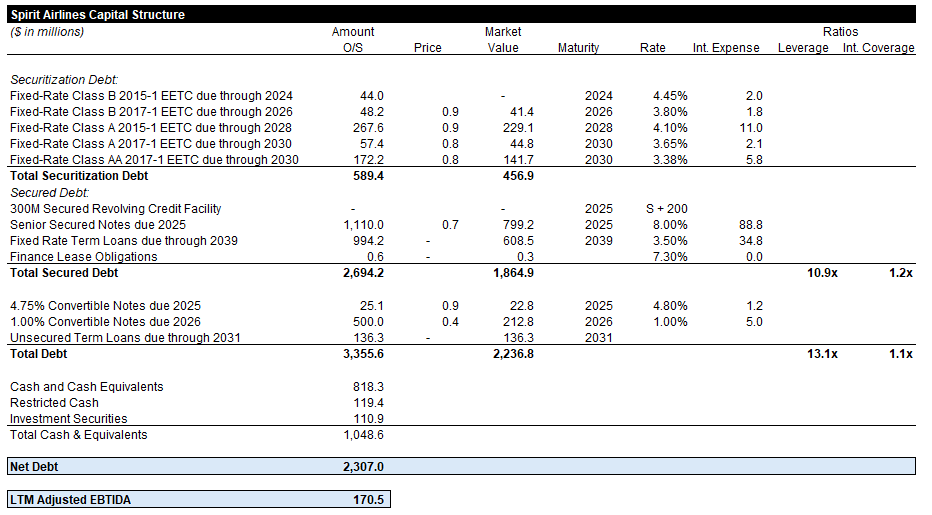

With the merger off the table, Spirit finds itself in a precarious financial position. This is evident in the significant drop in their stock price following the DOJ ruling, with shares plummeting by over 70%. What initially started as a strategy for Spirit to strengthen its domestic dominance in 2022, ended up as a desperate attempt to alleviate their capital structure issues. As depicted in Figure 7, Spirit is burdened with a debt of over $3.3bn, with lower pieces in the capital structure trading at distressed levels. Despite boasting a robust liquidity of over $1bn, the airline industry's high capital requirements, coupled with an oppressive capital structure and an impending maturity wall in 2025, are expected to deplete Spirit’s cash reserves within 1-2 years.

With operating conditions proving to be difficult in 2023 and potentially in 2024, bankruptcy or some form of distressed exchange has become a real possibility, and the 8% Senior Secured Noteholders took this as an opportunity to strengthen their claim via a triple-dip.

Proposed Triple-Dip

To provide some brief context before digging into this situation, the triple-dip involved the 8% Senior Secured Notes due 2025. Upon the news that the Spirit/JetBlue merger was blocked, the 8% notes dropped 30 points, reaching a trading price of 48 cents on the dollar. Given that debt sitting above the 8% notes in the capital structure were also trading below par and an imminent liquidity/maturity crunch upcoming, it became likely that the 8% notes would either be fulcrum or below fulcrum if a restructuring were to occur, and that the 48 trading price was primarily driven via optionality. As Spirit hired Perella Weinberg Partners to seek restructuring alternatives, the bondholders, who knew that they had a double-dip already existing in the capital structure, hired Evercore as advisors as they believed they were entitled to a third claim. The reason the bondholders seeked this third claim, as we will explain later, is because the double-dip was being questioned for whether or not the claims should be treated as secured or unsecured. At the beginning of the value-fight, the 8% secured notes traded below 50, before quickly climbing to over 70 cents on the dollar. Currently, the bonds are trading just below 65 cents [2].

Now in any bankruptcy, the most common source of contention is over-collateral value. For airline companies, this is even more true. Airline collateral generally consists of 5 different categories: Aircraft (airframes and engines), Spare Parts, IP (branding, trademarks), Loyalty Programs, and Slots, Gates, and Routes (SGR). Typically, each collateral group has separate creditors with liens over those assets. As a result, there is often much infighting between secured creditors, especially those below the aircraft and spare parts level, as they challenge liens [5].

IP, Loyalty Programs, and SGR assets typically raise capital via IP financing, Loyalty financing, and SGR financing. The one we, and the 8% Senior Secured Noteholders, will focus on is the Loyalty Program financing.

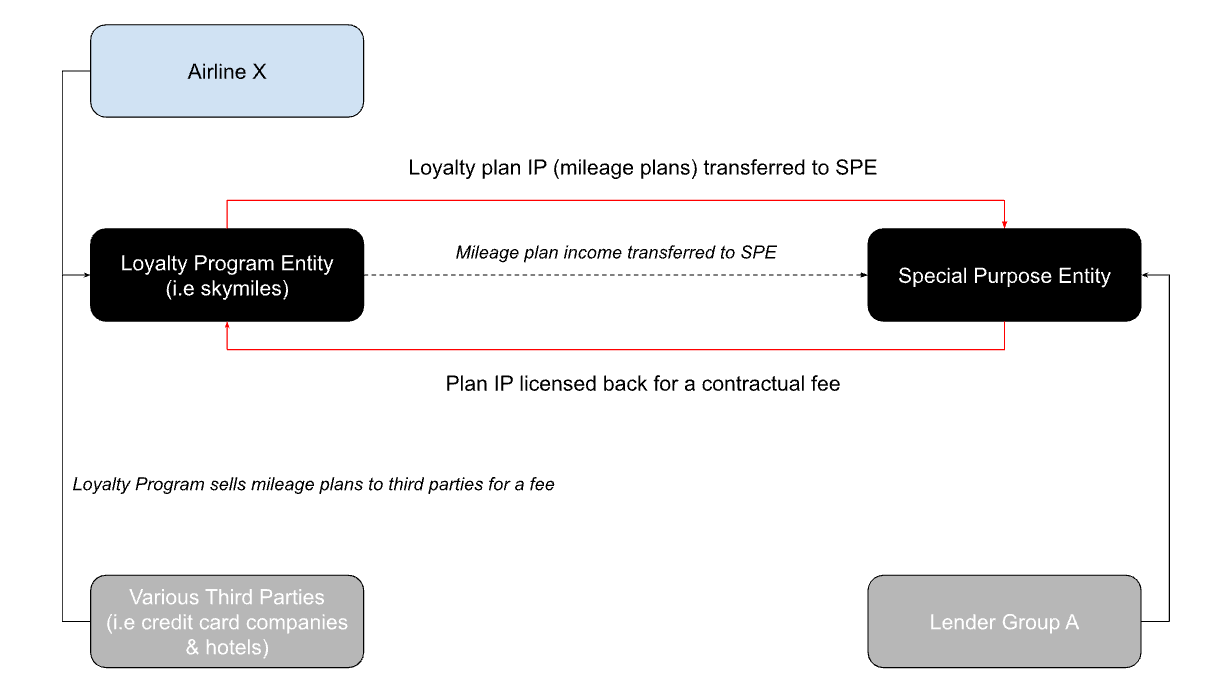

Loyalty Programs are often stored in a separate corporate entity (a subsidiary) of the airline. These programs are things like Delta’s SkyMiles. In a Loyalty Program financing structure, these loyalty program entities transfer the loyalty plan IP (i.e., the name/brand SkyMiles) to a special purpose entity. A special purpose entity (SPE) protects a parent company’s assets/liabilities and protection against bankruptcy. Once the loyalty plan IP is transferred to the SPE, the SPE then licenses the plan IP back to the loyalty program entity in exchange for a fee. Lenders will loan capital to the SPE and receive liens on the SPE assets (remember, this is the plan IP, the contractual fee, and potentially any equity interests) to secure the loans. Third parties (credit card companies and hotels) can purchase the miles (plan IP) from the loyalty program entity to add security and ensure that the SPE generates revenue. These third parties then issue these miles to customers at a contractual price. The revenue generated by the loyalty program entity is used to pay the license fee to the SPE, which provides extra security to help pay back lenders at the SPE level. The diagram below illustrates this structure [5].

The issue with loyalty program financing is that the mileage plan income to repay the loans is treated as an executory contract. Under the bankruptcy code, a debtor in bankruptcy can assume, assign, or reject any executory contracts. Thus, if the airline company or SPE were to file, the contracts could be rejected or renegotiated at incredibly unfavorable rates, effectively diminishing the claim's value. That said, let's evaluate the triple dip proposed in Spirit.

The triple dip involves the 8% Senior Secured Notes due in 2025. These notes are secured by the company's loyalty program and the brand IP assets. The noteholders, whose claims total $1.11bn, argue that the triple dip establishes a value of $2.85bn. These claims are subject to heavy negotiation, as some interpretations of the bond indenture have the 8% noteholders completely unsecured [3], [4].

The 8% Notes argued there were three claims in addition to their loyalty program and brand IP collateral [2]:

A $1.11bn intercompany loan to the Spirit parent company

A parent guarantee was provided to Cayman subsidiaries for all $1.11bn of debt outstanding

Claimed damages totaling $600mm of the brand IP license agreement

To understand the first and second dips, we will first examine Spirit Airlines' specific loyalty financing structure.

The loyalty bonds were initially issued in September 2020, totaling $850mm. As aforementioned, these loyalty bonds are secured by the loyalty program and brand IP. Referencing Figure 8, the plan IP was transferred to an SPE at a Cayman Islands subsidiary. In 2021, $340mm of these notes were redeemed; in 2022, an additional $600mm was added, totaling $1.11bn. These notes were backed by the 'plan IP income.' Specifically for Spirit, it was the royalty cash flow agreement with the Spirit parent company.

This financing structure involved an intercompany loan and a parent guarantee (two of the three dip claims). Let's look at the intercompany loan first. Under the bond indenture, when the notes were issued at the SPE, the net proceeds ($1.11bn) would be issued to the Spirit parent entity via an intercompany loan for day-to-day operations. The intercompany loan had an interest rate of 0.75% paid-in-kind. Additionally, the parent entity provided a guarantee that gave additional support for the loyalty bond lenders, assuming that the value of the plan IP does not cover the entire $1.11bn claim.

The final dip comes from termination damages relating to the brand IP license agreement. The bond indenture includes a clause that states that payments are owed, which equates to the present value of all future brand IP license fees, which has been stated at $600mm. If Spirit filed for bankruptcy, it would be an automatic trigger of this clause, and the 8% noteholders believe they are entitled to the full $600mm.

Strength of Case and Future Outlook

Despite the triple dip argued by the 8% noteholders, further analysis of the bond indentures demonstrates some flaws in this creditor group's argument.

There is no public credit agreement available regarding the intercompany loan, so there can be no certainty in this statement. However, these intercompany loans were unsecured for other loyalty financings for United Airlines and American Airlines. If this is the case for Spirit, this dip would likely be rejected in court.

Looking at the parent guarantee, it is hard to evaluate the full benefits of the guarantee until Spirit enters bankruptcy and we see this claim play out. The claim depends on excess value flowing to the parent so the guarantee can be upheld. However, Spirit's capital structure contains a variety of non-guarantor subsidiaries where the assets are held. Under the debt indentures, the claims at each non-guarantor subsidiary are entitled to full recovery before the value is provided to the parent company. In a reorganization scenario, it's hard to determine the exact value of these assets, and as a result, this parent guarantee is arguably another unsecured claim [2].

Finally, look at the damages claim from the brand IP termination. It is unlikely that this claim would receive any value in a bankruptcy scenario. This is because, unlike other claims, the damages claim arose circumstantially and has no security interest, which means it is effectively unsecured. This claim could increase the bondholder's position, but there may not be enough cash to cover it, and this 'additional' claim is likely to be added to the general unsecured pool [2].

This analysis shows that the 8% noteholders' claim would be treated as part of the general unsecured pile in a bankruptcy. However, much of the argument against the triple dip can be considered circumstantial, and the noteholders hold a legitimate threat of value leakage in bankruptcy. Thus, Spirit Airlines has hired Perella Weinberg Partners as debtor advisors to help with restructuring negotiations, and it is expected that an agreement between the debtor and the 8% noteholders will be achieved by the second half of 2024 [2].

Looking forward to future triple dips, it will likely require the innovation that we have seen in the Spirit case. Many professionals are calling the Spirit triple dip a double dip with extra credit support, and if true, proven triple dip has yet to be created in real-life [1].

Sources: [1], [2], [3], [4], [5], [6], [7], [8], [9], [10], [11], [12], [13], [14]

In case you missed the latest Pari Passu Newsletters:

Exciting Announcement: Our Merch Store is Finally Out

If you have a weird friend who enjoys looking at great companies with bad balance sheets all day, this is your chance to nail their next gift

How did you like this week’s Pari Passu? Loved | Great | Good | Meh | Bad

Looking to reach 13,500+ investors, bankers, lawyers?